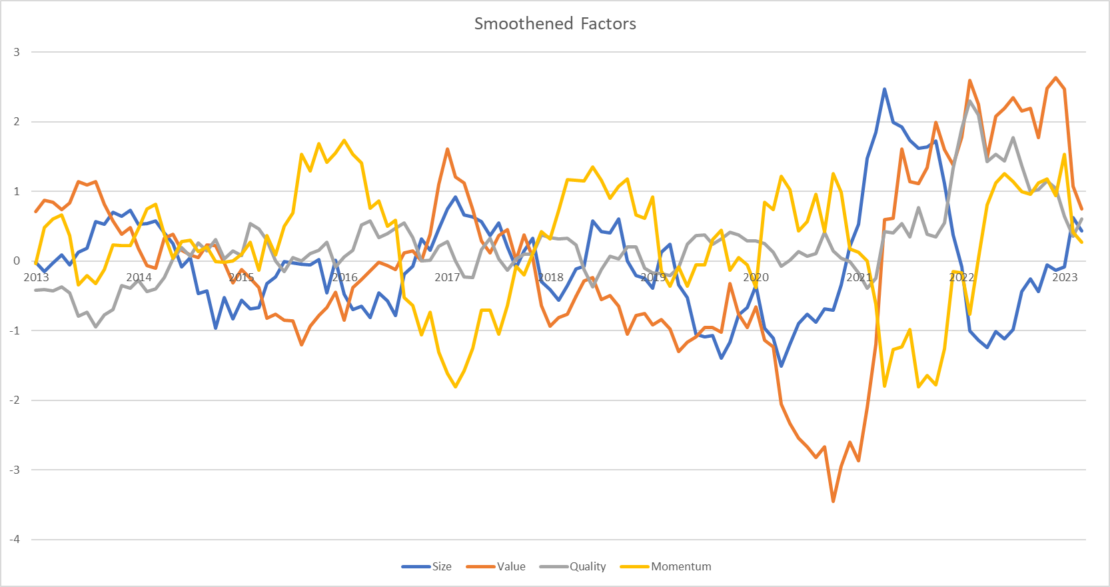

Factor investing is the basis for Everon’s investment strategy. The fundamental premise of this investment approach is to identify specific factors that explain asset returns beyond traditional market risk. These factors, such as Value, Momentum, Size, and Quality, have been widely studied and recognized as drivers of asset performance.

This article analyzes the recent developments in Value, Momentum, Size, and Quality factors using data from the Kenneth R. French Data Library. By doing so, it aims to provide valuable insights regarding the dynamic nature of these factors and their potential impact on portfolio management and risk assessment.

Kenneth R. French is a researcher in the area of factor investing and provides precalculated factor data on his website. He became famous for the publication of the “Fama and French Three Factor Model” together with the Nobel Laureate Eugene Fama in 1992.

The factor data is constructed as long-short portfolios with the intend to extract the pure factor without effects driven by the market. This is the academic approach of factor construction and gives a good indication of the factor itself. However, in practice factors are used slightly differently in portfolio construction.

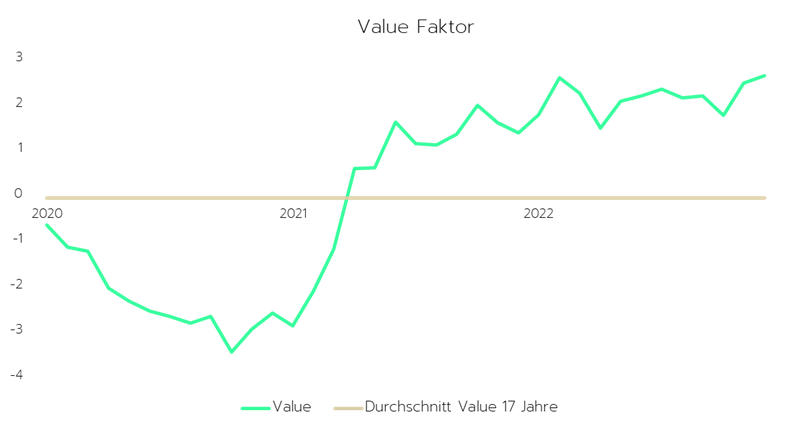

Value investing involves buying undervalued securities with the expectation that they will appreciate over time. The Value factor has historically been one of the most prominent factors in explaining asset returns, but has lost importance within the last decades. Recently, however, the Value factor has experienced a resurgence of interest, as investors question the sustainability of growth-oriented strategies in the face of changing market conditions.

Using data from the Kenneth R. French Data Library, the Value factor has exhibited a notable shift in recent years. From 2015 to 2019, the Value factor underperformed, but in 2020 and 2021, it experienced a remarkable comeback. This can be attributed to several factors, including the market’s reaction to the COVID-19 pandemic, the subsequent economic recovery, and the reorientation of investor focus towards value-oriented strategies.

This orientation towards value remained strong in 2022, as the insecurity about the impact of the higher interest rate regime on the economy persisted. With the beginning of this year, we see already a shift back from value towards growth again. Even though the factor was on average negative for the last decade, value is still the go-to factor in times of crisis. Therefor it should still find its consideration in an asset managers investment decision.

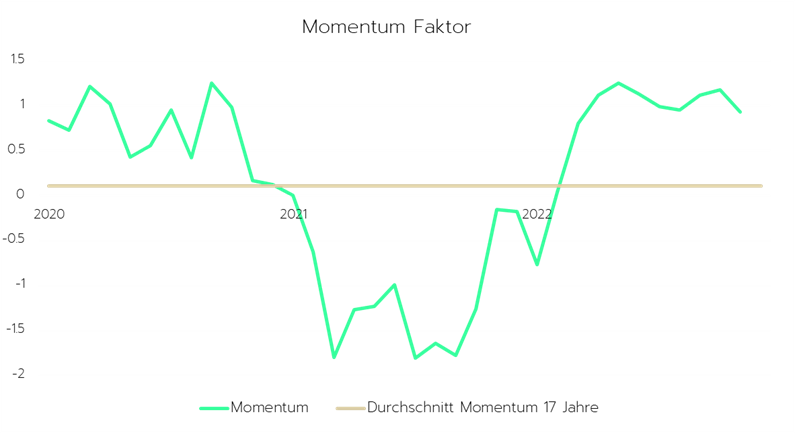

Momentum Factor

Momentum investing involves taking long positions in assets that have exhibited strong recent performance and short positions in assets that have underperformed. The Momentum factor is based on the notion that assets with strong past performance tend to continue outperforming in the short term. The Momentum factor has been well-documented in academic literature, and it has been a popular strategy among both individual and institutional investors.

The Momentum factor has been relatively consistent over the past decade with a positive premium on average. Despite short-term fluctuations, the Momentum factor has generally maintained its ability to generate excess returns for investors. However, the factor has experienced some periods of underperformance, such as during the market turmoil induced by the COVID-19 pandemic.

Especially when markets exhibit high volatility with fast change of directions, momentum becomes instable. Since mid-2021 to the end of 2022, momentum was a strong factor, but with the tech rally in the first months of 2023, the overall momentum factor weakened again.

Size Factor

The Size factor, also known as the small-cap premium, posits that smaller companies tend to outperform larger companies on a risk-adjusted basis. This factor has been extensively studied and has shown to be a persistent driver of asset returns. However, the Size factor has experienced some fluctuations in recent years, raising questions about its long-term stability.

The Size factor has shown mixed performance over the past decade. While small-cap stocks have generally outperformed large-cap stocks, the premium associated with this factor has diminished in recent years.

Several explanations for this trend include increased competition among investors, better access to information, and improved risk management practices. However, during the recovery in 2020/21, Size was an outperformer compared to other factors. Data suggests that Size is especially attractive during times of economic recovery.

Quality Factor

The Quality factor focuses on companies with strong fundamentals, such as high return on equity, low leverage, and stable earnings growth. Quality investing has gained prominence in recent years, as investors seek to mitigate risk and identify companies with sustainable business models. The Quality factor has been shown to be a valuable addition to multi-factor portfolios, offering diversification benefits and potential for outperformance.

The Quality factor has performed well over the past decade, with a generally stable premium. This suggests that the Quality factor has been relatively resilient, even during periods of market turmoil such as the COVID-19 pandemic.

The strong performance of the Quality factor can be attributed to various factors, including investors’ increasing focus on companies with sustainable business models, greater emphasis on environmental, social, and governance (ESG) factors, and the recognition of quality as a source of long-term value creation.

Implications Investors

The analysis of the Value, Momentum, Size, and Quality factors provides valuable insights for asset managers and investors seeking to capitalize on factor risk premia. The following points summarize the key takeaways from this study:

Value: Despite a period of underperformance, the Value factor has experienced a resurgence in recent years. Asset managers should remain vigilant and adaptive to changing market conditions to capitalize on the potential return premiums associated with this factor.

Momentum: The Momentum factor has generally been consistent in generating excess returns, but it is not immune to short-term fluctuations and periods of underperformance. Investors should understand the potential risks associated with Momentum investing and incorporate appropriate risk management strategies.

Size: The Size factor has shown mixed performance in recent years, with the small-cap premium diminishing over time. Asset managers should remain cautious in their reliance on the Size factor and consider potential changes in its efficacy when constructing portfolios.

Quality: The Quality factor has demonstrated strong and stable performance, suggesting its resilience and potential for long-term value creation. Investors should consider incorporating the Quality factor into their investment strategies to enhance portfolio diversification and capitalize on the benefits of quality investing.

Changes in factors over time:

Graph shows the factors’ 12-month simply moving average to correct for short term fluctuations. Data used from Kenneth R. French Library.

We have seen that factors evolve differently over time and perform differently during specific market environments. Correlations between the considered factors suggest, that it is beneficial to combine them as some exhibit negative correlations to each other.

By doing so, the outperformance of one factor can make up the underperformance of another factor. If we then continue to apply weightings to the factors according to their short-term momentum, we can even minimize the impact of the underperformance by some factors in order to achieve an overall superior result.

Market

Size

Value

Quality

Momentum

Market

1

0.347

0.082

-0.568

-0.326

Size

0.347

1

0.272

-0.222

-0.363

Value

0.082

0.272

1

0.183

-0.181

Quality

-0.568

-0.222

0.183

1

0.111

Momentum

-0.326

-0.363

-0.181

0.111

1

Correlation is calculated based on the smoothed data. Data used from Kenneth R. French Library.

Conclusion

The development of factor risk premia, particularly for the Value, Momentum, Size, and Quality factors, has significant implications for asset managers and investors. By closely monitoring the evolving relationships between these factors and adapting the investment strategy accordingly, asset managers can better manage portfolio risk and potentially improve investment performance.

As markets continue to evolve, understanding the dynamics of factor risk premia will remain crucial for successful portfolio management and risk assessment in the field of factor investing and beyond.

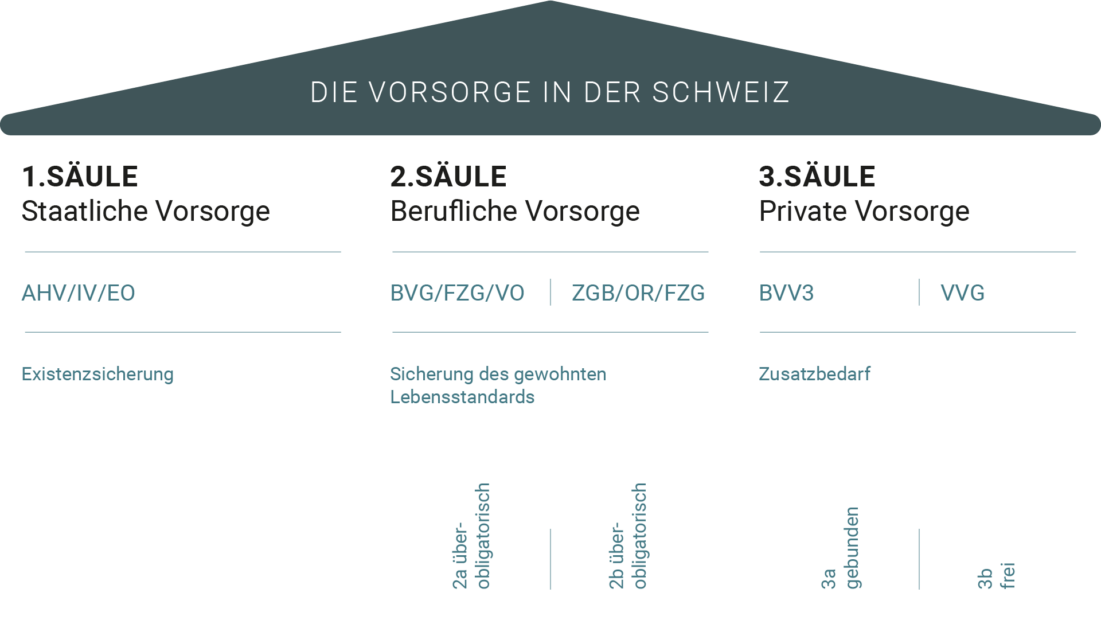

All about occupational benefits in Switzerland’s 3-pillar system

People who live and work in Switzerland pay part of their income into the financial instruments of the first and second pillars. In addition, the Swiss pension system allows people to make voluntary retirement contributions with partial tax incentives.

As the second pillar, the occupational pension plan (BVG) is an important pillar of the Swiss 3-pillar system. It complements the mandatory AHV insurance. But how far do the benefits go and to what extent do they cover actual needs in old age?

In this guide, you will find answers to questions about the BVG contribution obligation, the possible amount of the old-age pension and the additional safeguards. This will enable you to classify the options in concrete terms and pursue your personal pension strategy in a targeted manner.

The BVG pension supplements the retirement pensions of the first pillar and provides additional coverage in case of disability and death.

Every employer maintains a pension fund or is affiliated with one.

Employees are compulsorily insured from a minimum income.

Employerscontribute at least 50 percent of the monthly contributions.

The expected retirement pensions from the first and second pillars are not sufficient to secure the standard of living in old age.

What is BVG? The legal basis

In colloquial language, the abbreviation BVG is often used in Switzerland to refer to occupational pension plans, i.e. pension funds. BVG stands for «Federal Law on Occupational Retirement, Survivors’ and Disability Pension Plans». This law sets out the framework for occupational pension provision. The federal law has been in force since January 1, 1985.

Pension funds existed in Switzerland many decades earlier. As early as 1925, about 262’000 members were insured in 1’200 pension funds. However, membership was reserved for only a few citizens, such as civil servants or bank employees.

BVG: 2nd pillar of the 3-pillar system

The Swiss pension system is based on three pillars, which explains the classification of the BVG:

First pillar: state pension (AHV)

Second pillar: occupational pension plan (BVG)

Third pillar: private pension provision (see tips on pillars 3a and 3b)

The second pillar (BVG) helps insured persons and their dependents with benefits in retirement, disability and death.

Pillar 2a and Pillar 2b

The second pillar of the Swiss pension system is divided into a compulsory and a non-compulsory part. The insurable income in the BVG is limited in its amount – the obligatory part. For the part of the income above this, the extra-mandatory part, private provision can be made with the pension instruments of pillar 2b.

The importance of the BVG in the context of pension planning

The mandatory pension covers various risks.

These include:

Protection in old age (BVG pension)

Accidents

Disability

Death

Daily sickness benefit insurance to ensure continued payment of wages in the event of illness

Vested benefits institutions are also components of the BVG.

With regard to coverage in old age, the goal of the BVG is that the pension income together with the AHV pension should cover about 60 percent of the last income.

Employers take over organization and share in contributions

As with AHV contributions, employers contribute at least 50 percent to occupational pension plans (BVG). Employers are also responsible for organizing and paying the contributions. As an employee, you therefore receive coverage through a pension fund and do not have to worry about the details.

BVG mandatory ensures minimum benefits

The federal law (BVG) contains regulations that pension funds must comply with. This means that as an insured person, you are guaranteed minimum benefits by law.

Every employer has a pension fund

To ensure that every employee has the option of occupational benefits, all employers must maintain appropriate pension funds or join a joint scheme. Even if the employer fails to do so, employees are guaranteed to be insured with the Stiftung Auffangeinrichtung BVG. This acts as a safety net for the second pillar on behalf of the Confederation. Vested benefits that cannot be transferred to any other institution are also paid there.

Safeguards for the vicissitudes of life guaranteed by law

Since the BVG stipulates the safeguards for survivors in the event of disability or death, insured persons enjoy uniformly prescribed minimum benefits. For example, insured persons with a degree of disability of 70 percent or more receive the full pension and those between 40 and 69 percent receive a partial pension.

Old-age pension only covers part of income

If you take a look at the exact regulations for the old-age pension, you will quickly recognize the gaps within the coverage provided by the BVG.

For this purpose, it is important to be informed about the following restrictions:

Compulsory insurance only from BVG minimum annual salary: employees are subject to compulsory insurance from an annual salary of at least 22’050 francs (as of 2023). This means that there is no insurance for lower incomes and therefore no pension entitlement is built up.

Insurance limited to maximum amount: Up to an annual salary of 88,200 francs is provided for retirement. For incomes above these income limits, private pension provision is therefore existential.

Self-employed persons are not compulsorily insured.

Employees with fixed-term employment contracts are not insured: This applies to employment contracts of up to three months.

Family members on one’s own farm are not insured.

People with reduced earning capacity (at least 70 percent) are not insured.

The limitations on coverage make it clear that in the course of a person’s working life, almost everyone is not insured for more or less large amounts of income. This means that there will be even more gaps in coverage in old age if no private provision is made for this.

The BVG obligation: From when and who is obliged to pay contributions?

According to the BVG, employees are required to pay insurance if they are already insured in the first pillar (AHV) and earn at least CHF 22’050 (as of 2023).

Compulsory insurance begins as soon as an employment relationship is entered into. The minimum age is 17 years of age. Until the age of 24, the contributions only cover the risks of disability and death. Only then are the contributions used to save for the old-age pension.

Important: As mentioned in the previous section, some groups of people are not compulsorily insured (self-employed persons, temporary employment contracts, family members in the agricultural business, disabled persons).

Voluntary insurance via the second pillar (BVG)

Those who are not compulsorily insured under the BVG may be able to take out voluntary insurance.

Part-time work: If you earn below the BVG minimum wage of 22’050 Swiss francs (as of 2023), it is possible to be insured as a voluntarily insured person with the Stiftung Auffangeinrichtung BVG.

Self-employed persons: As a self-employed person, you have the option of taking out voluntary insurance with your professional association, with the pension scheme of your employees or via the Stiftung Auffangeinrichtung BVG.

Calculation and payment of contributions

The employer, who also pays the BVG contributions, takes care of the connection to the pension fund. According to the BVG, at least half of the contributions must be paid by the employer. Employees have their share deducted directly from their monthly salary.

The BVG minimum contribution is regulated in ascending order according to age groups in the BVG.

Age

BVG contribution

25 – 34

7 percent of insured salary

35 – 44

10 percent of insured salary

45 – 54

15 percent of insured salary

55 – 65

18 percent of insured salary

Employers may make higher contributions than required by law to retain their employees.

Coordination deduction and insured salary

According to the framework law BVG, the benefits that insured persons receive from the first and second pillar are coordinated. Therefore, a so-called coordination deduction is made in the income to arrive at the insured salary. This currently amounts to 25’725 francs (as of 2023) and corresponds in principle to 87.50 percent of the highest AHV full pension.

For example, if an employee has a gross annual salary of 79,000 francs, this results in an insured salary of 53’275 francs (79’000 – 25’725). The contributions are again calculated from the insured salary. It is therefore important for your pension planning to note that not the entire salary is insured.

Minimum insured salary

The coordination payment would lead to a situation where low incomes would no longer be insured. To avoid this, the legislator has defined a minimum insured salary, which in principle corresponds to 150 percent of the maximum AHV full pension (CHF 2’450, as of 2023). The minimum insured annual salary is therefore CHF 3’675 (as of 2023).

Upper BVG limit and maximum insured salary

The upper limit of the gross salary to be insured under the BVG is three times the maximum AHV full pension (29’400 francs, as of 2023). This results in a BVG limit of 88’200 francsin 2023. In this context, pay attention to the benefits of your pension fund, as some pension funds provide higher benefits than the BVG stipulates.

The maximum insured salary is calculated from the upper BVG limit and the coordination deduction. This is an essential limit for the personal pension plan. For 2023, this means that a maximum of CHF 62’475 of the salary is insured.

Save taxes as a self-employed person with a voluntary pension plan

If you belong to a pension fund as a self-employed person, you can deduct BVG contributions of up to 25 percent of your annual income subject to AHV from your taxable income, depending on your pension plan.

Vested benefits in the event of an interruption of the employment relationship

By nature, insured persons do not remain members of the same pension fund throughout their working lives. In the event of a change of employer, the retirement assets are taken over by the new pension fund. However, even if a new employment relationship does not follow seamlessly, the pension fund assets paid in may not be withdrawn from the pension circuit. This is the case, for example, in the event of maternity or unemployment. The previous pension fund then transfers the termination benefit to a catch-up institution after 24 months at the latest (after six months at the earliest). Providers include various banks, wealth management companies or insurance companies.

The vested benefits institution holds the capital in a low-risk vested benefits account. Since it hardly generates any return there, you should, if necessary, examine alternative securities solutions, such as those offered by digital asset management offered by digital asset management companies.

The BVG pension: ordinary withdrawal

The ordinary withdrawal of the BVG pension is scheduled as soon as the retirement age is reached.

You have the following options for drawing the retirement assets:

monthly pension upon reaching retirement age

Withdrawal of the balance as a lump sum

Withdrawal of a quarter of the balance as a lump sum and the rest as a pension

Please note that the options for lump-sum withdrawals are regulated differently in the pension funds. It is therefore advisable to look into this issue about ten years before you retire.

BVG pension and AHV pension together should cover about 60 percent of the last net income. However, this frequently found generalization is not accurate in many cases. Note that due to the limits described in the previous sections, it can be assumed that the complete income is rarely insured during the working life.

Early Retirement Option

With many pension funds, it is possible to withdraw assets as early as the age of 58. Early retirees must expect deductions of between three and five percent per year of early withdrawal.

Personal circumstances answer the question of pension or lump sum

Since the decision cannot be reversed, it must be made very carefully and, in the case of married couples, jointly.

To help, the following table shows a comparison of the main differences.

Pension

Capital

Income

Regular income is secured for life.

The income from the assets develops depending on the capital market and the investment strategy.

Flexibility

The withdrawal of the fixed pension is unchangeable.

Free decision on investment and use of the capital. The strategy can be adjusted if life circumstances change.

Survivors’ pension

Widow’s or widower’s pension normally 60 percent of the retirement pension drawn. Cohabiting partners and adult children are not included in the statutory provision.

Existing assets can be disposed of by will within the framework of the statutory provisions.

Taxation

The pension is fullytaxable.

One-time capital benefit tax at a reduced tax rate. The existing capital is taxed as assets, the income from it as income.

With regard to individual circumstances, for example, the state of health is a criterion for deciding between pension and capital. Those who expect an above-average life expectancy will opt for annuities.

Spouses also often prefer to opt for a pension in order to provide for their spouse. People without a life partner are more likely to opt to bequeath part of the pension fund capital to descendants.

Risk tolerance and experience with investments also influence the decision for or against a lump-sum withdrawal. If you have sufficient other sources of income , you can invest the capital profitably, for example if you have experience with securities investments.

When making a lump-sum withdrawal, pay particular attention to the following points:

Pension funds have deadlines by which the lump-sum withdrawal must be declared.

Married couples and registered partnerships: written consent of the partner is required.

In the case of purchases into the pension fund, the resulting benefits cannot be made before three years after the last purchase.

Use the professional support of an asset management company.

Pension or lump sum: combination often the best choice

A combination of annuity and lump-sum withdrawal can often be a suitable option. If the accumulated retirement assets are high, it may make sense to split them into an annuity portion and a lump-sum payment. The pension portion can then be used to cover current expenses, while the lump-sum payment can be used for additional needs such as travel or major purchases. In this way, you can benefit from the advantages of both options and have both regular income and greater financial flexibility.

The BVG pension: early withdrawal

Under clearly defined conditions, the BVG also permits an advance withdrawal of the saved capital before retirement age.

Construction or purchase of residential property: Provided the home is owner-occupied, the pension fund assets can be withdrawn early for the construction or purchase of residential property. Mortgage loans can also be repaid with the capital.

Self-employment as main occupation: In the year in which you start working as a self-employed person, you can withdraw your pension fund assets early. However, this is always in full, i.e. not as a partial withdrawal.

Leaving Switzerland for good: Emigrants can make advance withdrawals from the mandatory occupational pension plan if they emigrate to a non-EU/EFTA country . In the case of EU/EFTA countries , the advance withdrawal does not work, as here the mandatory insurance for old age, disability and survivors’ benefits takes effect and this, according to the law, prevents the advance withdrawal.

Valuable safeguards of the BVG

The main insurance benefits of the BVG include disability and survivors’ benefits.

Disability benefits

A disability pension is paid from a degree of disability of 40 percent. The amount is graduated according to the degree of disability and starts at 25 percent of the full pension at 40 percent disability. The full disability pension amounting to 6.8 percent of the projected retirement assets is paid for a degree of disability of 70 percent or more.

Survivors’ pension

The BVG provides for a survivor’s pension if the deceased leaves dependent children. Likewise, the surviving spouse receives a widow’s or widower’s pension if the deceased is 45 or older and the couple were married for at least five years. In the event of remarriage, there is no further entitlement to a survivor’s pension. If the requirements are not met, the surviving spouse is entitled to a lump-sum settlement of three annual pensions.

Since January 1, 2007, surviving registered partners have the same entitlements under the BVG as spouses. The prerequisite is that the partnership existed for at least five years before the death and that joint children are to be maintained. However, it is important to check whether the respective pension fund has already included these benefits in its catalog.

The amount of the survivor’s pension is 60 percent of the retirement pension drawn (or the full disability pension, if applicable).

Divorced spouses may also be entitled to a survivor’s pension. Prerequisites: The marriage lasted at least ten years and a pension or lump-sum settlement was awarded in the divorce decree.

In addition to the surviving spouse, also Children of the deceased are also entitled to a BVG pension. This is paid to the children until they reach the age of 18 and amounts to 20 percent of the old-age pension. Provided the child is still in education or is at least 70 percent disabled, the orphan’s pension can be drawn until the age of 25.

The BVG pension in practice: examples

The amount of the BVG pension depends on the retirement assets you have built up with your pension fund at retirement. To determine the pension, the retirement assets are multiplied by a fixed conversion rate. For example, if you have retirement assets of 250’000 Swiss francs, this results in an annual BVG pension of 17’000 Swiss francs or 1’416 a month at a conversion rate of 6.8 percent (as of 2023).

The retirement assets are calculated from the following items:

Retirement credits (contributions from employee and employer)

Pension funds must pay interest on the credits and benefits paid in at a minimum interest rate. This has steadily declined in recent years due to the persistent low interest rates and has been as low as 1 percent since 2017 (as of 2023). Until 2002, it had been 4 percent since 1985. This development makes it clear that a reliable projection of the old-age pension is not possible. Added to this are the changed mandatory insurance sums as well as the conversion rate, the reduction of which from 6.8 percent to 6 percent is already being discussed by Parliament .

In order to provide an initial orientation despite the uncertain parameters in the future, the following are therefore some rough calculation examples, which are primarily intended to illustrate the differences in the various case situations. As part of your personal pension planning, make sure to update your individual projections on an ongoing basis and adjust them to reflect changes in the underlying conditions.

Please note in the examples that the calculations are based on assumptions from the past as well as in the future, which may not apply in your personal case.

Example 1:

30-year-old

Career entry at age 25

Annual salary: CHF 80’000 (average salary until age 65)

insured salary: CHF 54’275

Contribution (as a 30-year-old today 7 percent): CHF 316

of which share as employee: CHF 158

Pension after retirement at 65: CHF 1’440

Example 2:

45-year-old

Career entry 25

Annual salary: CHF 110’000 (average salary until age 65)

insured salary: CHF 62’475

Contribution (as a 49-year-old today 15 percent): CHF 780

of which share as employee: CHF 390

Pension after retirement: CHF 1’690

In addition to the BVG pension, a pensioner’s child’s pension may be payable if the insured person dies (including early retirees). It is paid in the amount of 20 percent of the retirement pension, but not more than for children up to the age of 18. If the child is still in education, a maximum age of 25 applies.

Even though the examples cannot be used to derive a personal projection due to the constantly changing parameters, the differences in the income brackets become clear. In the examples, a gross salary that is 30’000 francs higher only accrues a further pension entitlement of around 3’000 francs or 250 per month.

The importance of the BVG within personal retirement planning

The occupational pension plan (BVG) is an important component of personal retirement planning in Switzerland. It forms the second pillar of the Swiss 3-pillar system and supplements the benefits of the first pillar (AHV). Disability and survivors’ p ensions are an essential financial aid in the relevant life situations.

However, you should not rely solely on the BVG to provide financial security in old age. After all, even if you have paid into it throughout your entire working life, in the best case scenario it will only provide you with around 60 percent of your former salary. As the sample calculations show, the coverage gap is particularly high for higher incomes.

It is therefore important to make use of the entire 3-pillar system and, in particular, to take advantage of allowances. In this way you benefit from Tax advantages and ensure that you are financially secure in old age and can maintain your accustomed standard of living.

Conclusion BVG: Valuable coverage for special life situations – not sufficient financial retirement provision

The occupational pension plan according to the BVG is an essential pillar of the Swiss social security system. The second pillar offers employees in Switzerland good financial security in old age and in the event of disability or death.

Pension funds are reputable institutions and they are financially sound. Employees have the option of increasing their pension benefits by making additional contributions and thus increasing their pension entitlements.

However, the pensions resulting from occupational pension plans, together with the state AHV pension, generally only secure basic needs in old age. However, the standard of living in Switzerland remains high by international standards. In this context, it is striking that despite the positive framework conditions in Switzerland, the Old-age poverty is above average in a European comparison. It is therefore important to take additional private pension measures in order to be able to maintain the accustomed standard of living in old age.

Switzerland is a country known for its high quality of life. As a Swiss citizen, it is therefore a desirable goal to enjoy old age in Switzerland. In this context, when you plan your financial future, the specific retirement age should not be missing from your considerations. There are many factors that influence the date of retirement in addition to the official regulations.

What retirement age can I currently assume and will the retirement date possibly change? Are there ways to plan for retirement before the official retirement age in Switzerland, and what do I need to consider?

Only those who know the rules regarding retirement age in Switzerland can optimally prepare for a comfortable and secure future. You will find the essential information in this article.

The long period until retirement offers a wide range of pension options.

Those who make optimal use of the long investment horizon until retirement age have an easier time of it.

The retirement age is currently rising in all countries.

Due to demographic developments and higher life expectancy, the financing of state pensions in Switzerland and internationally is reaching its limits.

Private pension provision is becoming increasingly important and is the instrument to help determine the personal retirement age.

The retirement age in Switzerland: today and in the future

Currently, there is a women’s pension age and a men’s pension age in Switzerland. This means that the following ordinary retirement ages apply for drawing an AHV pension:

for men 65 years

for women 64 years

History of the AHV: Controversial discussions about retirement age in Switzerland

The introduction of the AHV is undoubtedly a milestone within Switzerland’s social policy. It was introduced in 1948. The retirement age for men was set at 65. A retirement age of 65 was also set for women at that time.

Since then, there have been the following major changes during the further development of the AHV:

1957: After the pension had been increased several times since the AHV was founded, the women’s pension age was lowered by two years to 63. This revision followed the conviction that physical strength would decline faster in women than in men.

1964: Another AHV revision lowered the regular retirement age for women – this time to 62. At the same time, supplementary pensions for wives and children’s pensions were introduced, financed by a contribution from the state.

1972: Another milestone in Switzerland’s old-age provision was the introduction of the 3-pillar principle in this year. According to the constitution, the AHV pension is to ensure subsistence and is supplemented by occupational and private pensions.

1985: According to the constitution, pensions from the pension fund should ensure the «accustomed standard of living».

1997: With the introduction of income splitting, education credits and care credits as well as the widow’s pension, the retirement age for women was simultaneously raised again to 64 in several partial steps.

In the years that followed (2004, 2010 and 2017), there were repeated reforms sought in Parliament to raise the ordinary women’s pension age to 65. However, all reforms were rejected by the time of the people’s decision at the latest.

AHV 21 reform: Uniform retirement age for men and women

The people and the cantons approved the AHV 21 reform on September 25, 2022. On December 9, 2022, the Federal Council set the effective date for this at January 1, 2024.

Key points are:

The retirement age for women and men will be standardized (65 years). The continued financing of the AHV is secured until 2030.

The ordinary retirement age will in future be referred to as the reference age. This reflects the fact that flexible retirement between the ages of 63 and 70 is possible for both men and women.

Transitional arrangement

According to the reform, the reference age for women will be raised in several steps of three months per year, starting one year after the reform comes into force. If the reform comes into force in 2024, as currently planned, this means that women born in 1960 will not yet be affected by the new reference age. The 1961 cohort, for example, will then have a reference age of 64 years and three months. For the 1964 cohort, the reform will then be finally implementedin 2028 and the women of this cohort will have a reference age of 65.

Retirement age in Switzerland in international comparison

Demographic change and increased life expectancy are presenting many countries with enormous challenges. Even though trade unions and social welfare associations are campaigning for the lowest possible retirement ages, the question of financial viability is increasingly being raised. One consequence of this is often an increase in the statutory retirement age. With an age of 65, Switzerland is in the lower midfield in Europe.

For comparison, here are some countries with the respective statutory retirement age for drawing the full old-age pension:

Slovakia: 64 years

Austria: 65 years (currently transitional regulation, finally implemented for birth cohort 1968)

Germany: 67 years (currently transitional regulation, finally implemented for birth cohort 1964)

France: 67 years

Italy: 67 years

Denmark: 69 (currently transitional regulation, finally implemented for birth cohort 1967, thereafter increase according to the development of life expectancy).

A look beyond Switzerland quickly shows that an increase in the retirement age seems unavoidable. In Denmark, the retirement age has even been linked to the development of life expectancy. Experts therefore assume that it will already be at least 70 years in the next few years.

A reference age of 65 in Switzerland can therefore currently be seen as an expression of economic stability. However, Switzerland will not be able to ignore developments in the long term in order to continue financing the AHV system. This once again highlights the growing importance of occupational and private pension provision.

Early retirement: the options for early retirement

The AHV pension can be drawn one or two years earlier. For each year by which the pension is drawn early, you must accept a reduction of 6.8 percent. Important: The reduction is permanent. It therefore applies to the entire pension period. No children’s pensions are paid during the period of the early withdrawal.

An application must be submitted for the early withdrawal. The deadline for this is the end of the month in which the insured reaches the age of majority.

Usually no early withdrawal from the second pillar

Normally, the BVG pension, i.e. the pension from the second pillar, cannot be withdrawn early. However, some pension schemes allow early retirement from the age of 58. If you are interested, it is best to contact your pension fund at least one year in advance. Pillar 2b capital can, however, be withdrawn at any time.

Early withdrawal from the third pillar

You can withdraw capital from the third pillar at the earliest five years before the AHV retirement age. Please note that only one payment is possible – i.e. one full payment per pension account.

Pension deferral: When retirement is not yet an incentive

Early retirement is not attractive for everyone. So if you would like to continue working, you can postpone payment of your AHV pension for a maximum of five years. Working alongside the AHV pension is also possible.

If you postpone your AHV pension, you will receive a pension supplement later. This is graded according to the duration of the deferral and amounts to between 5.2 and 31.5 percent.

Usually no deferral of the pension from the second pillar

The pension from the occupational pension plan is normally paid from the normal retirement age. However, individual pension plans provide for deferral until the age of 70 in their regulations.

Deferral of benefits from the third pillar

If you can prove that you are working despite reaching the statutory retirement age, you can also postpone drawing from the third pillar for up to five years after the statutory retirement age. It should also be noted here that only one payment, i.e. the full capital, is possible.

Early retirement and pension deferral from 1.1.2024 (AHV 21 reform)

The standardization of the retirement age (in future «reference age») for men and women to 65 years will result in flexible retirement between 63 and 70 years. Women in the transitional years can already choose to retire at age 62.

At the same time, partial retirement and partial pension deferral will be introduced.

Instead of fixed reductions for early withdrawal and supplements for deferral, these will in future be based on average life expectancy. There will also be lower reductions for lower annual incomes (below CHF 57,360). The changes to the reductions and surcharges are planned for 2027 at the earliest. The rates should be set by the Federal Council shortly before they are introduced.

The Swiss pension scheme: Secure your financial future with the 3-pillar principle

The developments of the retirement age and the respective backgrounds clearly show that there will continue to be a shift within the three pillars of retirement provision in Switzerland. For future financial planning, it is therefore important to know and take advantage of the options within the 3-pillar principle.

First pillar: State pension plan

This consists primarily of old-age insurance and survivors’ insurance, known as AHV for short. In addition, there is disability insurance, unemployment insurance, maternity insurance and compensation for loss of income during military service. The first pillar represents a state-organized means of subsistence – but nothing more. Depending on the number of years of contributions as well as the contributions paid in, the maximum pension (as of 2023) is 2,450 francs per month for one person. For married couples, it is currently 3,675 francs.

The insurance covers all people who live or work in Switzerland, with or without gainful employment. Contributions are paid by employed persons and the amount depends on income.

Second pillar: occupational pension plan

The occupational pension plan is funded. It is divided into a

mandatory (2a) and

non-compulsory (2b) part

The compulsory part is the old-age provision (BVG pension). This part also includes daily sickness benefits insurance and accident insurance. It also includes vested benefits institutions to take over entitlements if the benefit provider changes.

Benefit providers of the second pillar are public as well as private pension funds. From a minimum annual BVG salary, employees are required to pay insurance and must pay contributions, half of which are paid by the employer. Self-employed persons can pay in voluntarily.

The insurance obligation only applies to a limited part of the income. The part above this is the extra-mandatory part. Voluntary provision can be made for this so-called precaution 2b. Tax advantages can be generated here, since both contributions and saved pension capital are tax-free.

The occupational pension plan can cover about 20 percent of the pension requirements. With the benefits from the first and second pillars, around 60 to 70 percent of the earned income can thus be covered, provided that the extra-mandatory insurances are also used.

As fewer and fewer working people will have to pay for more and more pensioners in the future, private pension provision will become increasingly important. Therefore, part of planning a financially carefree life in old age is the use of the third pillar.

The third pillar is divided into two areas:

Pillar 3a (tied pension provision, exempt from tax within certain limits, in exceptional cases, such as the purchase of a home, an advance withdrawal is possible)

Pillar 3b (free pension provision, no immediate tax advantages, fewer restrictions, flexible and needs-based coverage, flexible structuring of payouts)

Thanks to a wide range of financial products, the third pillar allows pension provision to be optimally adapted to individual needs. The identifiable gaps in coverage that are not covered by the first and second pillars of pension provision can be optimally closed with the third pillar. This is particularly relevant against the backdrop of the changing retirement age.

Thinking about tomorrow today: The advantages of early financial provisioning.

The earlier you start making financial provisions, the easier and more profitable it will be to achieve your goals.

There are several reasons for this:

If you start making financial provision in good time, you can determine your retirement in a more self-determined manner. This gives you more freedom and scope for development.

Early financial provision can offset the effects of lower pension and social security benefits.

Investing and saving early creates more wealth over time, and the compound interest effect is particularly powerful.

A solid long-term financial retirement plan helps realize financial goals and aspirations, such as buying a home or traveling the world.

Early financial provision creates the financial means to cope with unexpected expenses and emergencies, such as job loss, major repairs or illness.

Timely wealth accumulation allows for broad diversification and reduces investment risk.

A long investment horizon provides access to investment opportunities that may not be available at a later date.

Frequently asked questions (FAQ)

What needs to be arranged for retirement and when?

In order to receive an AHV pension, you must inform the compensation office in writing of your entitlement. The compensation office where you have paid AHV contributions in previous years is responsible for processing your claim. If you are unsure, your employer will inform you about the compensation office.

It is important that you submit your application no later than three months before you reach the statutory retirement age. This will enable the compensation office to obtain all the necessary information to calculate your pension.

To receive a BVG pension from the second pillar, you should contact your pension fund a few months before the regular retirement age. They will provide you with information on the exact amount of the pension and guide you through the necessary steps to receive it.

For benefits from the third pillar, you should also contact your private pension fund a few months in advance to find out about the modalities and the amount of your saved capital.

How is the amount of the pension calculated?

The AHV pension is determined by the years of contributions as well as the relevant average income. Additional education credits are granted for children and care credits are available for caring for relatives in need of care. Pensions are limited in terms of maximum pensions and minimum pensions. Insured persons can obtain an estimate of their OASI pension.

The BVG pension from the second pillar is calculated on the basis of the contributions paid in and the pension fund regulations. Normally, a one-time payment of a quarter of the capital is also possible upon retirement. The annuitization of the capital is based on a conversion rate, the minimum level of which is currently set by law at 6.8 percent. For a capital of 250,000 francs, for example, this means a pension of 17,000 francs a year, or around 1,416 francs a month, at a conversion rate of 6.8 percent.

The retirement assets from the third pillar are generally drawn as a one-time lump-sum payment.

Why is there old-age poverty in a wealthy country like Switzerland?

While the standard of living in Switzerland remains very high, the poverty rate in old age is increasing at a striking rate. This can be explained primarily by the fact that Swiss people are more dependent on assets in old age. This highlights the importance of using private pension options. According to statistics from the SFSO, the poverty rate for retirees who draw their main income from the first pillar is over 20 percent. However, if the main income comes from the second pillar, the rate already drops by more than half.

The topic of inheritance is complex and many are overwhelmed when they suddenly inherit higher sums of money or other assets. There are legal regulations that are supposed to regulate the transition. Nevertheless, there are also personal decisions to be made. How should the inheritance be managed and how can it be used or invested wisely? What should be considered when it comes to inheritance tax or debts?

As a testator, this guide will give you an overview of how you can ensure your own wishes. If you have inherited in Switzerland, you are also already prepared for the first steps.

Under Swiss inheritance law, the right to inheritance is based on the degree of relationship.

Testators can make provisions that deviate from the law of succession in a will.

Close relatives are entitled to compulsory portions, which may not be undercut even by their own dispositions.

Timely planning of the estate benefits testators and heirs.

Competent asset management helps to maintain and increase the inherited assets.

Parentel system: Swiss inheritance law regulates who inherits and how much

In Switzerland, inheritance law is determined by the parentetel system. If the deceased has not written an official will or inheritance contract, the degree of relationship determines who inherits and how much. With a will or inheritance contract, you can therefore document your will during your lifetime and avoid disputes among heirs.

Will: You draw up your will yourself and can also amend or revoke it at any time. You are free to formulate your instructions and regulations as long as you comply with the legal limits and, in particular, take into account the compulsory portions. Despite the will, the statutory inheritance law continues to apply due to the compulsory portions.

Inheritance contract: You and one or more of your heirs can jointly conclude an inheritance contract, which allows you to make decisions outside the legal framework and thus to make individual arrangements. These can only be changed or reversed if all parties agree.

Legal succession according to the parentetel system

The parentetel system determines who is entitled to receive an inheritance and the order in which they receive it. This system is ordered by degree of kinship. If there are no heirs in a particular parentel, the next closest parentel comes into question. Relatives from the third parentel are the last to be entitled to inherit.

First parentel: This includes direct descendants such as children, grandchildren or great-grandchildren. Children inherit in equal shares. In the case of deceased children, their descendants are entitled to inherit instead.

Second parentel: These are in particular parents. If they are deceased, their descendants inherit, i.e. siblings and, if applicable, nieces and nephews.

Third parentel: This is the trunk of the grandparents. Often the grandparents are already deceased and uncles, aunts and possibly cousins take their place. This is provided that there are no heirs within the first two parenteles.

Inheritance entitlement of the spouse

Spouses are always entitled to inheritance by law. The amount of the inheritance claim depends on the other possible legal heirs. In addition, the amount is also influenced by the property law chosen by the spouses.

The surviving spouse is entitled to:

If there are heirs of the first parentel: 50 percent of the inheritance

If there are only heirs of the second parentetel: 75 percent of the inheritance.

Determination of the estate

Before the inheritance is divided, the assets are divided according to matrimonial property law. If the spouses have not made any agreements in a marriage contract, the so-called ordinary matrimonial property regime applies. This means that the statutory regulations apply. A distinction is made between four different asset classes:

The assets brought into the marriage by the wife and gifts (own property).

The assets brought into the marriage by the husband (personal property)

Assets acquired by the wife during the matrimonial property regime (acquired property)

Assets acquired by the husband during the matrimonial property regime (acquisitions).

After this division, the surviving spouse is entitled to the following shares:

His/her own personal property

50 percent of his or her acquisitions

50 percent of the inheritance of his deceased spouse

The estate includes the remaining assets.

Spouses have the option of making agreements in a marriage contract that deviate from the legal requirements. For example, community of property or separation of property can be agreed. It can also be agreed in the prenuptial agreement that, for example, the surviving spouse is entitled to all the assets of both spouses in the event of the death of one spouse. However, the undercutting of compulsory shares is only possible in very few exceptional cases. One reason would be a serious crime committed by the heir against the testator.

Inheritance quota – compulsory portions – freely available quotas

When someone dies, the distribution of his or her estate is determined by the surviving relatives. In addition to the spouse, the children are also entitled to a certain compulsory share of the estate. The difference between the legally prescribed inheritance shares and the compulsory shares is the freely available quota, which can be assigned to beneficiaries by means of a will.

The table below provides an overview of the amount of the freely available quota in different family situations.

Heirs left behind…

Statutory inheritance quota

Compulsory part from the estate

Available quota

Descendants (first parentel)

100 percent

50 percent

50 percent

Spouse

100 percent

50 percent

50 percent

Spouse and children

Children 50 percent Spouse 50 percent

Children 25 percent Spouse 25 percent

50 percent

Spouse and parents

Spouse 75 percent Parents 25 percent

Spouse 37,5 percent Parents 0 percent

62,5 percent

One parent and siblings

Parent 50 percent Siblings 50 percent

Parent 0 percent Siblings 0 percent

100 percent

Inheritance tax: The cantons always inherit in Switzerland as well

In Switzerland, the cantons are responsible for determining the inheritance tax. The canton in which the deceased had his or her last residence is responsible. The cantons also decide on tax exemption rules, such as allowances. Inheritance tax is generally payable by the heirs.

Inheritance tax and inheritance tax

Inheritance tax has two forms: inheritance tax and inheritance tax. The inheritance tax taxes all the assets of the deceased without regard to the individual heirs. The inheritance tax taxes each heir’s share of the estate according to his or her relationship (degree of kinship) to the deceased. In Switzerland, only Solothurn and Graubünden still have an inheritance tax. However, the municipalities there can also demand an inheritance tax.

Inheritance tax rates and exemption amounts of the cantons

The different tax laws in Switzerland make the assessment of inheritance tax complex. In general, the tax rate is progressive and certain allowances are taken into account depending on the degree of kinship. Thus, close relatives are entitled to higher allowances than distant ones.

For spouses, no inheritance taxes are due in all cantons. The same applies for the most part to descendants. Only in Appenzell Innerrhoden, Lucerne, Neuchâtel and Vaud do children have to expect low inheritance taxes of 0.01 to 3.5 percent.

For parents, the range in the cantons goes from pure tax exemption to a tax rate of fifteen percent. However, there are also tax-free amounts of up to 50,000 francs.

Depending on the canton, siblings can expect an inheritance tax of up to 23 percent, with allowances of up to 30,000 francs.

Tax rates for other heirs range from 12 to 49.50 percent, depending on the canton, and there are only small allowances.

Tax on inheritances abroad

In principle, there is a risk that the inheritance will be taxed by several countries. This may be the case, for example, if the deceased person or an heir resided abroad or if an inherited property is located abroad. In these cases, it must be clarified which law applies to the inheritance. In order to avoid heirs having to pay taxes more than once, Switzerland has concluded double taxation agreements with some states in which this is avoided.

Inheritance in Switzerland: the essential steps after death

After the death of a person, the relatives have to deal not only with the mourning but also with the inheritance matters. Those who know the most important points will save themselves some excitement. The following are therefore the essential steps.

Submitting a will: As soon as you find a will, you must submit it to the authorities. The assessment of authenticity or correct compliance with formal requirements must also be left to the competent official body – this is what the law requires. In this respect, it is safest for the testator to file his or her will immediately with the appropriate office. Depending on the canton, this is the municipal administration, the district court, the inheritance office or the official notary’s office.

Opening of the will: As a rule, the will is opened by the authorities within one month. This means that the will is read to all heirs present. For the opening, the office invites all legal heirs as well as those appointed in the will. From the day of the opening, many deadlines must be observed, such as the one-month deadline for filing an objection.

Apply for a certificate of inheritance: This is the legitimation for the heirs. Only with this certificate of inheritance will you, as the heir, have access to the assets. It is applied for at the same authority that opens the will.

Rejecting an inheritance if necessary: An inheritance does not necessarily have to be accepted. Sometimes heirs decide against accepting the inheritance for personal reasons. Concerns about having to assume responsibility for the decedent’s liabilities if the decedent was overindebted can also be a reason for disclaiming the inheritance. In such cases, the heir submits a written declaration of disclaimer to the court.

Securing the inheritance: The competent authority is obliged ex officio to take any necessary measures to secure the inheritance. In some cases, this may mean sealing the inheritance, taking inventory or ordering an administration of the inheritance. Sealing means blocking assets and is provided for in cantonal law for certain cases. In particular, if there is no agreement in the determination of the assets, the authority will take appropriate measures.

The community of heirs: If there are several heirs, they jointly form a community of heirs. Each individual heir has the right to divide the estate. Until the division of the estate, all heirs are joint owners. The co-heirs can exclude the division for a certain period of time. The testator can also exclude the division for a certain period of time in a decree. Likewise, the court has the possibility to postpone a division if this would be extremely unfavorable for the asset at the present time.

Agreement among heirs or action for partition: There is not always agreement among heirs, particularly with regard to the valuation of the assets. In principle, the valuation has to be made according to the market value, not only in the case of real estate. However, this is a complex procedure, for example in the case of companies. If no agreement can be reached, an action for partition is brought. In this case, the court takes over the objective division. In the end, the community of heirs is dissolved.

Inherited assets: What heirs should pay attention to now

The more extensive the estate, the more diversified it usually is. In addition to financial assets, the decedent may have owned a house, an apartment or even his own company.

Pay particular attention to the following points in relation to the estate:

Determine assets and debts: In principle, every heir has the legally guaranteed right to receive information about all of the decedent’s assets and debts. If the deceased has appointed an executor in his or her will, the executor is obliged to provide all heirs with comprehensive information regarding the deceased’s assets. Even in the case of unclear property circumstances, heirs may request the preparation of a public inventory within a period of one month after the date of the deceased’s death. As already explained in the section on community of heirs, assets such as securities or real estate do not have to be liquidated immediately if this would currently only be possible with considerable losses.

Clarify pension fund assets: The beneficiaries are entitled to the claims from the pension fund assets after the death of the insured person. In most cases, there are spouses or orphans entitled to a pension and a survivor’s pension is paid. In all other cases, the pension fund regulations determine what happens to the pension fund assets. The regulations vary among pension funds. It is therefore possible for a saved capital to be forfeited and for it to benefit the community of insured persons.

Observe deadlines for declaration of disclaimer: Do you want to disclaim your inheritance due to overindebtedness of the testator or for other reasons? If so, you must submit a written declaration of disclaimer to the competent authority within three months of becoming aware of the death.

Financial planning for the inheritance: Unless heirs have the appropriate financial expertise themselves, they should take care of sound asset management in good time. Digital offerings today enable competent and at the same time cost-effective support even for manageable assets.

With appropriate preparation, testators avoid disputes in the event of inheritance

A carefully planned estate can help avoid conflicts and ensure that the testator’s last will is fulfilled.

Advance inheritance is one way in which parents, for example, can reduce their taxable assets during their lifetime and children can already take advantage of their inheritance. In addition, inheritance taxes can be saved if necessary. However, heirs with an advance withdrawal must have the advance withdrawal offset against their inheritance. Although children, for example, may thus be treated unequally, the compulsory portion may still not be undercut.

In order to document one’s own will, a will is a central matter. Important: Spouses each need their own will. Although a will cannot completely avoid legal difficulties, it simplifies matters. To ensure that your will is taken into account in the event of incapacity, you should also consider a living will and an advance directive.

One way of donating your assets to a social or charitable purpose is to set up a foundation. This can help ensure that heirs can use the assets in a dignified manner after the deceased’s death.

Family businesses sometimes suffer from the fact that succession is not precisely regulated. Anyone wishing to preserve their life’s work should therefore plan in good time during their lifetime.

In this context, the legal structure of the company plays a major role, as it can affect inheritance tax and tax treatment. It is therefore highly recommended to consult with an experienced expert in order to consider the legal and tax consequences.

Separated spouses should know that even in the event of separation, intestate succession applies. If this is not desired, it can only be excluded by divorceor in part by a prenuptial agreement.

Conclusion: Ensure one’s own will for the estate with planning during one’s lifetime.

Death and inheritance are unpopular topics during one’s lifetime, and people like to avoid them. However, problems arise at the latest in the case of inheritance, when disputes arise among the heirs. Frequently, however, unresolved inheritance issues already lead to disputes and disadvantages during one’s lifetime. This can be the case, for example, in the case of an unresolved company succession, as a result of which the development of the company and thus the preservation of the assets can ultimately suffer.

A correctly and unambiguously drafted will, a living will and an advance directive are the appropriate means of planning the estate at an early stage and documenting one’s own will. The clarity of the regulations and clarification with the family ensures the testator’s will and minimizes the potential for conflict. Particularly in the case of larger estates, a lawyer with expertise in Swiss inheritance law should therefore be consulted. In addition to legal clarification, heirs should think about appropriate financial planning for the estate at an early stage. Today, the financial market offers competent asset management services for almost all sizes.

It has been a turbulent few weeks for the global banking sector. Triggered by the bankruptcy of Silicon Valley Bank (SVB) and the liquidity problems of other US banks, this has now culminated in the takeover of Credit Suisse by UBS.

But how did it come about and what are the implications for wealth management? In this article you will find information.

A brief summary of what happened: Sillicon Valley Bank in the U.S. recently ran into liquidity problems as a result of sharp interest rate hikes by the Federal Reserve. The bank’s problem was that it had invested a large part of its customer balances in long-dated U.S. government bonds, which are virtually considered a risk-free investment. However, these investments lost massive value due to the sharp interest rate increases last year, which exacerbated the long maturity of the securities.

In addition, the bank’s customers, which are increasingly young technology companies, increasingly withdrew their customer funds due to the current difficult economic environment. When it then became known that the bank had to sell bond positions at a large loss, a bank run ensued.

In the back of the mind that Credit Suisse already suffered from major problems and outflows of money last year, the events in the US now ensured that CS also saw massive withdrawals of funds, which ultimately led to it having to be taken over by UBS.

Impact on asset management

Here we see another good example of the fact that trust is a fundamental factor in this sector. Since this trust has been shaken among many, we would like to use the current occasion to discuss the possible impact of such a crisis on asset management.

Custodian Banks: The first point of contact between a crisis, such as that of Credit Suisse, and wealth management would be if the latter were used as a custodian bank. However, asset managers often work with multiple banks, regularly evaluating whether the relevant partner banks are still an appropriate place to hold client assets.

Securities as special assets: Securities held in custody at a bank that is experiencing financial difficulties are considered to be so-called special assets. This means that these assets may not be used to pay off creditors of the bank. This means that your securities are protected at all times.

Independence: Asset managers are usually not banks themselves and can act completely independently and therefore do not get into liquidity problems, even if all clients want to withdraw their assets. This also means that the asset manager will change custodian bank as soon as it becomes apparent that the financial situation of the respective partner bank is not good.

Impact on securities prices: A banking crisis can of course have an impact on securities prices, in the banking sector itself but also outside of it. We have seen this happen in recent weeks, when shares in banks that had nothing to do with the current situation have fallen massively in value. Your asset manager has an eye on current market events at all times and can often better assess how great the danger is for an existing securities portfolio. This makes it easier to distinguish whether it is a short-term reaction of the market or whether there is a need for action because fundamental economic factors have changed.

As you can see, asset managers are not completely immune to crises in the financial sector either. However, they help to better identify risks and act accordingly, minimizing the potential impact. Furthermore, your asset manager will advise you to spread your existing assets in cash across several banks. As in the case of Credit Suisse, we have seen that the actual loss of client assets is very unrealistic.

Now, one might say that this is only the case if the bank is appropriately large. However, smaller banks in particular have a much lower-risk business model than large banks, as they are not active in the high-risk business areas. Some banks also specialize entirely in holding customer assets in custody and facilitating securities trading, which in turn poses little liquidity risk.

While client assets are secured by the UBS takeover, the real losers are Credit Suisse’s investors and the reputation of the Swiss financial center.

Questions? We are here for you!

If you have any questions about this topic or would like to learn more about how we work with our client assets, we are always available to help. Simply get in touch with us.

The Swiss Residential Property Price Index (IMPI) allows you to track the ongoing development of real estate prices. These have almost doubled since 1998. Even in recent years, from the fourth quarter of 2019 to the fourth quarter of 2022, the index has risen from 100 to around 115 points. So is it worth investing?

Investing in real estate in Switzerland is therefore particularly worthwhile if you have a long-term investment horizon. Swiss real estate is one of the investment forms that offer a high degree of inflation protection. Returns are generated through both rental income and capital appreciation. There are many ways to invest in Swiss real estate – directly or indirectly.

So first get an overview of whether and in what way Swiss real estate fits your personal investment strategy.

Real estate is considered a security component of a balanced investment strategy.

Owning your own home is a physical investment that is already being used today.

Direct investment in real estate requires expertise and time.

Personal requirements determine the pros and cons of a real estate investment.

With indirect investments, it is possible to invest in real estate even with small amounts and little effort.

Expected returns vs. secure living in one’s own home

The first step in examining the personal advantages and disadvantages of a real estate investment is to clarify your initial situation:

Do you already own a property?

Do you live in your own property or rent?

What significance does the saved rent have for you in the context of old-age provision?

What financial assets do you have and in which asset classes are you already invested?

When you invest money in real estate, you own a physical asset. Provided you occupy the property yourself, you are already using this asset. This is a clear difference from investing in securities, for example. Owners of their own home often do not consider their property from a yield perspective. They rate the value of being able to make independent decisions within their own four walls, of being able to design their own home and of being safe from termination of the tenancy very highly. Do you see yourself in this or is it more important for you to be able to keep housing costs low in the long term?

Basically, part of a balanced investment strategy is to have a certain amount of financial assets before investing directly in a pure income property, i.e. a property for renting out. After all, when you purchase a property directly, you are opting for a long-term investment. Compared to securities, it cannot usually be converted into liquid assets at short notice, should the need arise. Also, the not inconsiderable incidental costs of acquisition must first be earned through subsequent returns.

Investing money in real estate: Pros and cons

From an investor’s point of view, real estate offers more than just security and income. There is also a risk in this asset class. The investment process also differs from other investments, especially when buying directly. Interested investors should therefore weigh the following advantages and disadvantages.

The main advantages include:

Real estate in Switzerland has been characterized by a steady increase in value in the past.

Investments in real estate are considered a stable value investment and inflation protection.

Compared to other forms of investment, real estate is subject to only minor fluctuations in value.

Rented properties provide a regular source of income.

The saved rent on an owner-occupied home eliminates a significant burden in old age.

An owner-occupied property is an investment that can already be experienced today (free design, high living comfort).

Possible disadvantages are:

The purchase prices of real estate in Switzerland are very high, even in international comparison. For example, the median price per square meter in the largest Swiss cities is around 12,000 Swiss francs, which is about twice as high as in the largest cities in neighboring Germany.

Real estate should generally be viewed as a long-term investment. The ancillary costs of acquisition must first be earned through corresponding income from the property. At the same time, the equity capital invested is tied up for the long term.

The decision-making process and the purchase process require a relatively large amount of time.

Maintenance and repairs require the formation of reserves and represent a financial risk.

Mortgages for financing may be subject to interest rate risks.

Although returns on real estate have been mostly steady in the past, they have been lower compared to other investments.

Taxation of residential property in Switzerland

If you own your own home, you pay federal and cantonal taxes on the imputed rental value (“Eigenmietwert”) in the form of fictitious income. The imputed rental value is between 60 percent and 70 percent of the average market rent. If you rent out your property, the actual rental income is taxable.

Conversely, homeowners have the interest on mortgages and maintenance work deducted from their taxable income. Thus, those who own a heavily mortgaged property benefit from this rule, as the interest payments are usually higher than the imputed rental value. In contrast, those who live in their debt-free home are disadvantaged, as they must pay income taxes on the full imputed rental value.

When a property is sold, there is predominantly a profit that must be taxed – real estate gains tax is due. The net profit is taxable. Expenses incurred during the purchase and sale can therefore be deducted. The longer the real estate owner has held his property, the lower the tax burden. Therefore, those who purchase a property and sell it again at a profit a short time later pay the most.

Lucrative investment in real estate – also for me?

The advantages of real estate investments listed above do not necessarily apply to every investor. Likewise, depending on your personal situation, not all of the disadvantages mentioned will be perceived as such. Therefore, answer the following questions for yourself. This will help you to quickly determine whether real estate is a suitable form of investment for you or not. Successful real estate investors are usually those who continuously take care of their property. In comparison, investing in an ETF, for example, requires very modest effort.

Can I imagine investing my money for a longer period of time and not being able to dispose of it during that time?

When acquiring a property, there are not inconsiderable ancillary acquisition costs. The value of the property must initially increase by this amount so that you do not have to sell at a loss. Also note that you cannot plan the optimal time for a sale.

Can I imagine taking on a lot of debt?

If you want to invest successfully in real estate, you should not be afraid of high debts. Hardly anyone can finance the purchase of a property from equity alone. Furthermore, in the case of rented properties, it is advisable to finance a larger portion for tax reasons.

Am I able and willing to cope with the possible interest rate risk of the financing?

The installments for the mortgage rarely remain at the same level until repayment. After the fixed interest rate expires, the bank will offer a market interest rate that is current at that time for the follow-up financing. So you should be prepared for fluctuations.

Am I willing to invest my free time in searching for and viewing real estate?

A successful real estate investment depends in the first step on finding the suitable property. In addition to expertise, this requires a great deal of time.

Can I imagine carrying out necessary renovation or modernization work and paying for the costs?

Investors with manual skills have a clear advantage here. In any case, you must always think about building up a reserve for necessary repairs and renovations.

Do I want to take care of the rental and management or hire someone to do it for me?

The ongoing management of a property involves just as much effort as the upcoming new rental. Investors who have a certain relationship to their property will find it easier. Otherwise, consider the financial outlay for property management.

Can I financially afford not to rent out an apartment?