The so called “60/40-portfolio” is a classic. The combination of 60 percent stocks and 40 percent bonds in a portfolio, was seen as very favorable in risk-return relations. The main assumption behind it is that stocks and bonds exhibit a low, if not even negative, correlation over time. Therefore, historical correlations between stocks and bonds have been a subject of interest for investors seeking to diversify their portfolios.

Understanding these correlations provides valuable insights into asset allocation strategies and risk management.

This article will explore the historical correlation between stocks and bonds in the U.S., discuss factors influencing these correlations, and highlight recent trends and their implications for investors.

Contents

Historical Perspective: A look into the past

The relationship between stocks and bonds has not always been consistent. There have been periods when the two asset classes have moved in the same direction and periods when they have moved in opposite directions. In general, bonds have served as a hedge against stock market losses due to their typically low historical correlation to stocks, at least over the last 25 to 30 years. When we look over a longer horizon, there was a regime of largely positive stock and bond correlation between 1945 and 1995.

This was for instance the case in 1969 when the Federal Reserve hiked interest rates to curb rising inflation, which led to both stocks and bonds moving in a negative direction. This scenario happened again in the last year, when stock and bond returns fell after the Federal Reserve increased interest rates at the fastest pace in 40 years. Over four decades, this simultaneous drop has occurred only 2.4% of the time across any 12-month rolling period.

Factors Influencing the Correlation

Several factors can influence the correlation between stocks and bonds. One of the significant drivers is interest rates. Higher interest rates can reduce the future cash flows of these investments, hurting both stock and bond returns. Bond prices are directly linked to the interest rate level and their valuation drops with an increase in interest rates, as long as their coupon payments are fixed. The reason is that existing bonds with old (low) coupons become less attractive compared to newly issued bonds with higher coupons.

Stocks are impacted because higher interest rates mean higher financing costs and an intentional slowdown of the economy. Both effects tend to reduce company profits and therefor lead to lower equity valuations.

Additionally, the level of risk appetite among investors also plays a crucial role. When the economic outlook is uncertain and interest rate volatility is high, investors are more likely to reduce risk in their portfolios, pushing down both equity and bond prices. Conversely, if the economic outlook is positive, investors may be willing to take on more risk, potentially boosting equity prices. Also consider that the attractiveness of cash increases with the interest rate level of a currency as it can already provide decent “riskless” returns.

Reading tip: Investment strategy in focus: The power of income strategy

Recent Trends and Implications

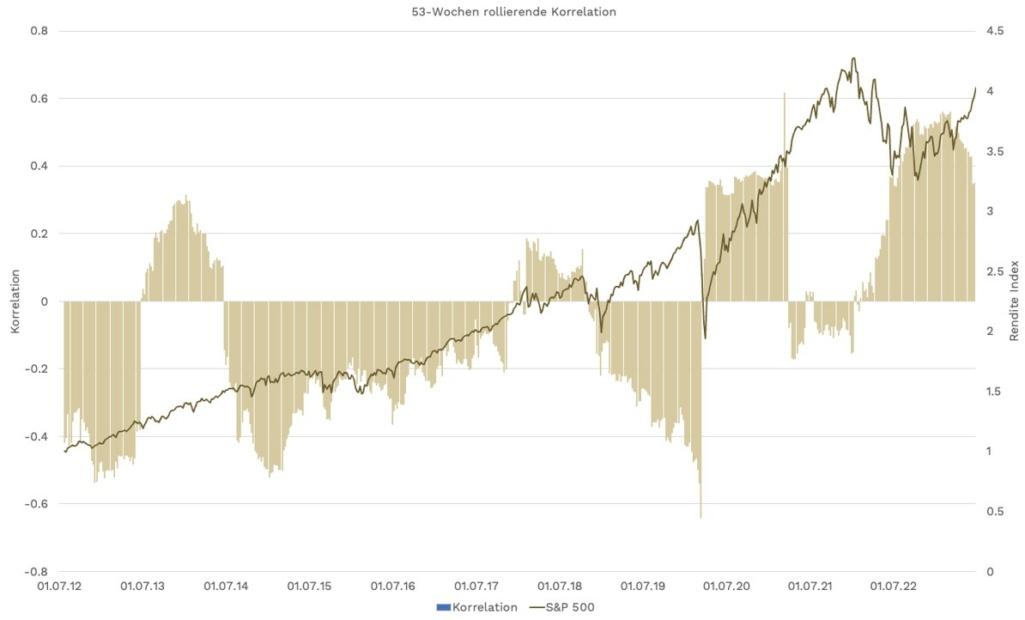

We look at the US equity and bond markets, represented by the S&P 500 and the Bloomberg US Aggregate. As shown in the below graph, the rolling 53-weeks-correlation between bonds and stocks was negative most of the times between 2012 and 2020. So, over this period, the diversification effect of stocks and bonds worked well. However, the 60/40-portfolio was not a very attractive investment from a return perspective, as the zero-interest rate regime introduced very low yields on fixed income investments.

In recent years however, a notable shift has occurred in the stock-bond correlation and in the attractiveness of fixed income. In 2022, there was a lockstep movement between the S&P 500 and Treasury bonds. This was driven largely by high inflation, restrictive Fed statements, stubbornly high consumer spending, and nominal wages, which frequently upset the bond market.

This led to a situation where stocks often fell when interest rates rose, challenging the diversification benefits of traditional 60/40 portfolios, but boosting yields for fixed income investments.

As we move into 2023, the investing landscape appears to be changing. Weak manufacturing data, a softening household employment picture, and tame 3-month annualized inflation gauges suggest that the U.S. economy may move towards a mild contraction at times during the year.

This could lead to softer interest rates and a shift in the correlation between stocks and bonds, with Treasury bonds potentially moving in a different direction from equities. If this shift occurs, it would likely benefit diversified portfolios, particularly given the higher starting yields in Treasury bonds compared to previous years.

Moreover, the investing climate may begin to resemble the period between 1945 and 1995, where stocks and bonds often moved together in a high-growth, sustained inflation environment. This would mark a significant shift from the period from the late 1990s through the early part of the COVID-19 pandemic, where deflation was more of a concern than high inflation, promoting the benefits of diversification between stocks and high-duration Treasury securities.

Reading tip: Investing money in Switzerland: investment strategies and the 1×1 of investing

The Impact of the COVID-19 Pandemic

The COVID-19 pandemic also played a significant role in influencing the correlation between stocks and bonds. The Federal Reserve’s shift to unprecedented monetary stimulus in response to the pandemic led to a unique situation in the bond and equity markets.

The U.S. stock market rebounded from the initial shock of the pandemic and reached new highs, fueled in part by the low interest rates that made bonds less attractive. Meanwhile, the Federal Reserve’s commitment to keeping rates at near-zero levels led to a surge in bond prices, resulting in a rare period where both bonds and equities performed strongly (period from mid 2020 to mid 2021).

Reading tip: Factor risk premiums: Value, Momentum, Size and Quality in recent years

Conclusion

While the correlation between stocks and bonds has varied over time, understanding this relationship and the factors that influence it is crucial for investors seeking to diversify their portfolios and manage risk.

As we move into 2023, it remains to be seen how this correlation will evolve. However, given the current economic trends and the higher starting yields in Treasury bonds, diversification could potentially prove more beneficial in the coming year1.

Today, financial markets are experiencing sharp swings as the implications of higher interest rates become more apparent. Yet, it’s important to remember that, over the last century, cycles of high interest rates have come and gone, and both equity and bond investment returns have been resilient for investors who stay the course5.

While the correlation between stocks and bonds will continue to shift based on various factors, what remains constant is the importance of a well-diversified, balanced investment portfolio. Investors who understand these shifts and adapt accordingly can better navigate the ever-changing financial landscape.