Many people dream of living a self-determined life in old age and securing their future financially. Saving with the third pillar can be the right way to achieve this.

The tax-privileged pillar 3a serves as private provision for retirement. For this reason, restrictive regulations have been put in place with regard to Pillar 3a payments and, in particular, early withdrawals. Thus, the early withdrawal is only possible in a few exceptions and under strict conditions.

In this article, we explain the different situations in which an early withdrawal from the 3rd pillar is possible. We also discuss taxation in various cases so that you know what to look out for.

Contents

- 1 The most important facts at a glance

- 2 When can I start drawing Pillar 3a benefits?

- 3 Early withdrawal and lump-sum payments from pillar 3a strictly regulated by law

- 4 What should I bear in mind when withdrawing from pillar 3a?

- 5 Optimize taxes with pillar 3a withdrawals

- 6 Frequently Asked Questions (FAQ)

The most important facts at a glance

- As a rule, withdrawals from pillar 3a are made five years before and a maximum of five years after the normal retirement age.

- There are strictly regulated exceptions for early withdrawal of pension assets.

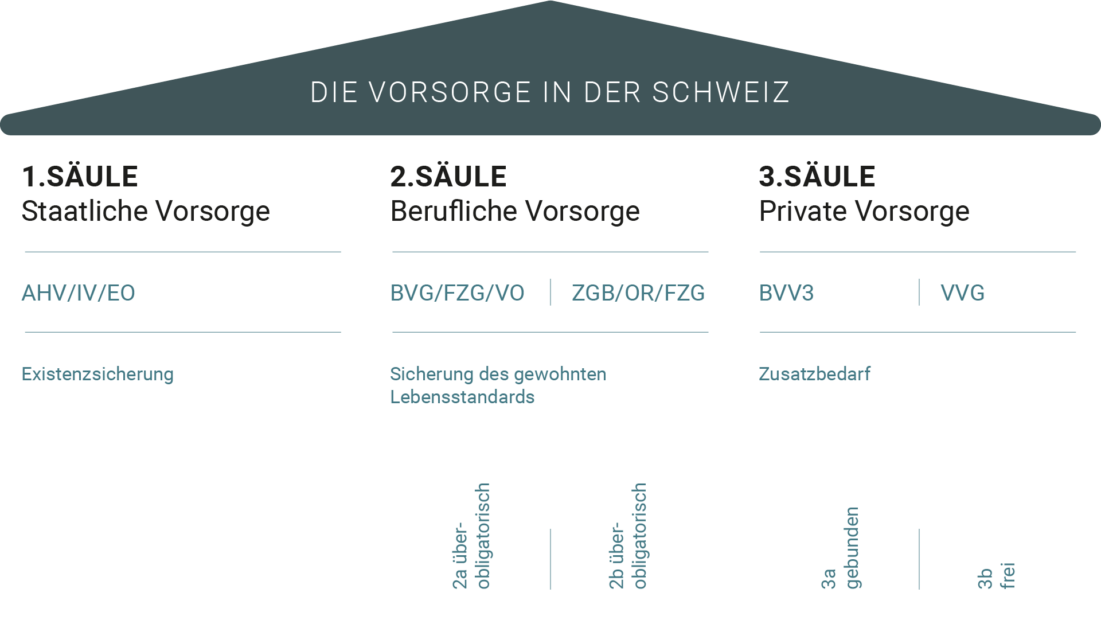

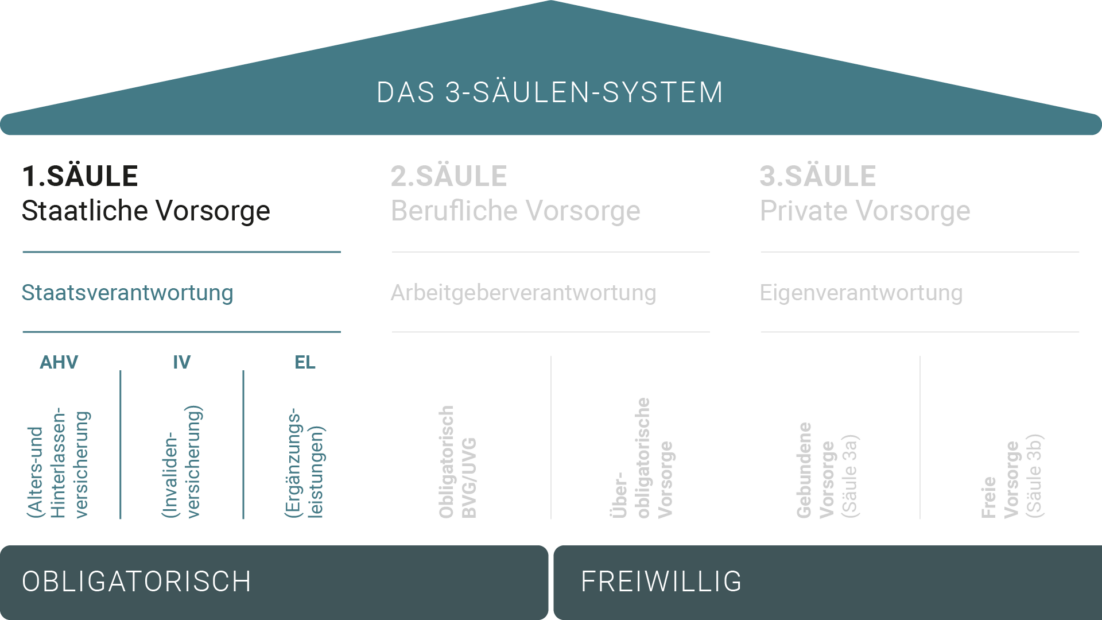

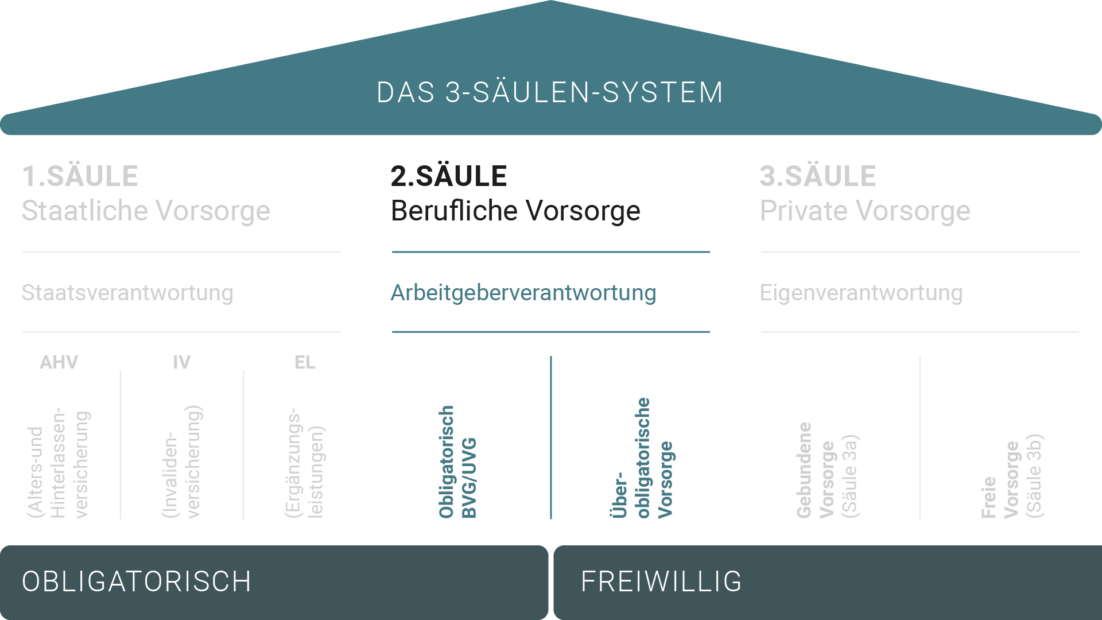

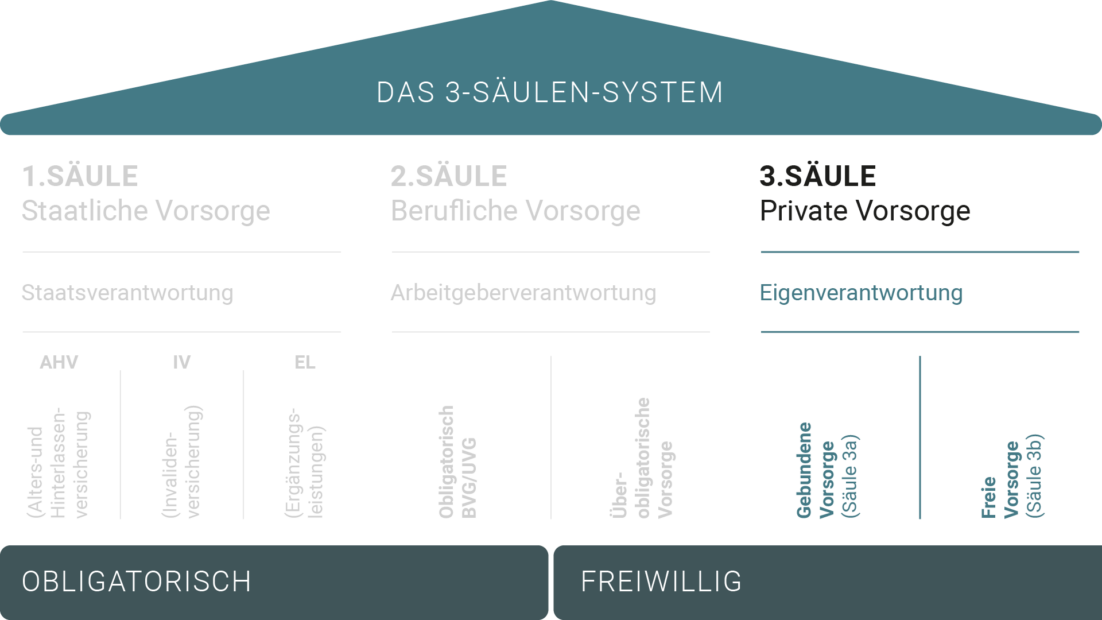

- Pillar 3a is the tied pension plan for Swiss citizens and is tax-subsidized by the federal government.

- In pillar 3b (free pension plan), the contributions cannot be deducted for tax purposes and the credit balance is taxed as assets. The amount paid out, on the other hand, is tax-free and the timing can be freely chosen.

- For pillar 3a, the maximum amount that can be paid in in 2022 has been set at CHF 6,883. People who do not have a pension fund may pay in up to 20 percent of their earned income, up to a maximum of 34,416 francs.

When can I start drawing Pillar 3a benefits?

Pillar 3a can be drawn five years before reaching the regular AHV retirement age. This is (as of 2022) at age 64 for women and 65 for men.

Pillar 3a capital can also be drawn after retirement. If you continue to work after you have reached the regular retirement age, you can postpone the withdrawal. However, as soon as you stop working or no later than five years after reaching the regular retirement age (69 or 70 years old, respectively), the capital must be withdrawn.

These options for withdrawal during retirement are also referred to as ordinary withdrawal.

Early withdrawal and lump-sum payments from pillar 3a strictly regulated by law

The early withdrawal is only possible under some specific circumstances, which are regulated by law. These strict regulations were enacted because the intent of the tax-advantaged Pillar 3a is to provide for personal retirement.

The following circumstances allow for early withdrawal of Pillar 3a benefits:

Leaving Switzerland

If you leave Switzerland permanently, you can have your retirement capital paid out early. In the case of married couples, the written consent of the spouse is required. Proof of the new permanent residence abroad must be provided.

Self-employment

Self-employed persons who do not belong to a pension fund can have the capital from the 3rd pillar paid out in the first year. However, this is only possible for partnerships and not for legal entities, such as a stock corporation or limited liability company. If you are self-employed, you can pay a higher annual amount into the third pillar to compensate for the lack of a second pillar.

Self-occupied residential property

It is possible for you to obtain additional personal funds for the purchase or construction of a permanently owner-occupied home by making an early withdrawal of saved Pillar 3a funds. An early withdrawal of pension capital is possible every five years. The payout is subject to a reduced tax rate. Taxes may vary depending on the place of residence and the volume of the payout.

Pillar 3a capital can also be used to pay off mortgage loans. With an early withdrawal from Pillar 3a, there is also the option of investing in residential property and financing renovations and value-enhancing investments.

The following applies when you make an early withdrawal of Pillar 3a capital:

- There is both no age limit and no minimum withdrawal for early withdrawals from pillar 3a. Withdrawals that come from Pillar 3a to finance real estate are considered “real equity” (unlike pension fund withdrawals).

- In addition to purchasing residential property, you can also use the early withdrawal to repay a mortgage debt.

- It is only possible to withdraw a partial amount of the Pillar 3a capital up to five years before reaching regular retirement age. After that, you can only draw on the entire amount of the respective pension plan. Therefore, it is worthwhile to maintain different pillar 3a accounts.

Disability

Recipients of a disability pension from the IV who do not have disability coverage can have their money paid out from pillar 3a.

Death

In the event of the death of an insured person, the capital is paid out. The order of persons entitled to the payout is as follows: Spouse, children as well as persons for whom the deceased provided a significant living, parents, siblings as well as other heirs.

Purchase of pension fund

The capital of the 3rd pillar can also be used to buy into a tax-exempt pension fund. The requirements for this are

- there are no contribution gaps

- there is no early withdrawal for home ownership that has not been repaid.

What should I bear in mind when withdrawing from pillar 3a?

Regardless of when you want to withdraw your money from Pillar 3a, you must actively dissolve the Pillar 3a. The bank or insurance company from which you receive the money does not automatically dissolve the pillar for you. Make sure that you contact your bank in time. They will send you the application form. If you do not get in touch, the bank will contact you. Important: You must declare the Pillar 3a withdrawal in your tax return. Income tax is levied separately for the withdrawal at a reduced rate.

Here are some important points to consider when making a Pillar 3a withdrawal:

- Pay attention to taxation of pillar 3a withdrawals: You must always close a 3a account in full. It is not possible to make partial withdrawals from a pillar 3a account – unless you have several 3a accounts. This must be taken into account when coordinating withdrawals from the various pillars of retirement provision. In addition, married couples will have their withdrawals added together within the same tax period.

- Coordinate withdrawals with the pension fund: The withdrawals you receive from the 3a pillar should be coordinated with possible withdrawals from your pension fund. Capital that you withdraw from the 2nd and 3rd pillars in the same year is added together when calculating the capital payment tax. If you choose a staggered withdrawal, the tax will be lower.

- When a new 3a account is still profitable in the last year of work: If you plan to retire at regular retirement age and receive all or only part of the pension fund assets as a lump sum, you should close your existing 3a account a year earlier. Otherwise, the pension fund capital drawn and the 3a payouts count together for tax calculation purposes. As a result, the lump-sum withdrawals will be subject to a higher tax rate. You can then still open a new 3a account for the last year.

- Late closure of the 3a account: 3a assets must be withdrawn as soon as you reach your regular AHV retirement age. Provided you can prove that you will continue to work, you can continue your pillar 3a for up to five years. During this period, you can continue to make contributions.

Optimize taxes with pillar 3a withdrawals

Tax progression is the keyword when optimizing taxes. In order to keep the progression as low as possible, it is advisable to open several 3a accounts and distribute the retirement assets among them.

Depending on the overall situation, the individual accounts can be closed from the age of 60 (men) or 59 (women) over several years. The respective tax is calculated per year and is based on the account closed in the same period.

As a result of this individual assessment, the progressions at the federal level and, depending on the canton, are lower overall than if you were to close all accounts at the same time. This is a simple way to save several thousand francs in taxes.

Example:

Daniel and Maria, who both live in the city of Zurich, are the example here of the advantage of staggering the payment of several accounts over several tax periods.

- Daniel has his accumulated pension capital totaling 473,506 Swiss francs paid out on his retirement at age 65. This incurs around 51,000 Swiss francs in taxes, which are collected jointly by the federal government, the canton and the municipality.

- Maria has also saved a total amount of 473,506 Swiss francs for her retirement provision. However, this amount is divided between two accounts that she had opened some time ago. Maria has her two accounts paid out in two different years. Each has a balance of CHF 236,753. Due to the different payout dates in two years, her tax burden is reduced to a total of CHF 31,000 – even though she, like Daniel, lives in Zurich.

By staggering the payout of her 3a capital from several accounts, spread over different years, Maria has saved over CHF 20,000 compared to Daniel.

Frequently Asked Questions (FAQ)

When should I deal with Pillar 3a and the payout?

The earlier you start looking at Pillar 3a options, the more efficiently you can design your retirement savings. Because of the possible tax advantages when distributing payouts and in order to coordinate the payout with the pension fund, you should initiate the necessary steps at least one year before withdrawal.

What role does the investment mix play?

The low-interest-rate policy has meant that savers hardly receive any interest on their invested capital. It is true that retirement savings deposited in a 3a account earn better interest than normal savings accounts. But the interest rate granted by the banks is very low overall.

It is worth investing in 3a securities funds. Equity funds in particular yield much higher long-term returns than 3a savings accounts. Switzerland has strict regulations for 3a funds. Diversification is also regulated in this way. Depending on which 3a fund one chooses, the proportion of Swiss or global equities can be increased. Good diversification reduces the risk of losses in certain markets.

Is it possible to deposit and withdraw in the same year?

In the third pillar, there are no lock-in periods as known from paying into the pension fund. Consequently, it is possible to pay into pillar 3a in the same year in which you request a payout, regardless of whether you pay in first and then pay out or vice versa.

Continue reading in our journal: