Systematic Alternatives: How Rules-Based Multi-Asset Strategies Make Equity Portfolios More Resilient

Equities have formed the foundation of long-term wealth creation for decades. At the same time, they are regularly exposed to periods of significant turbulence, triggered by monetary policy turning...

Rising market concentration, uncertain inflation regimes, and unstable correlation structures are increasingly challenging classical diversification models. Systematic multi-asset overlays open new avenues for investors to structurally stabilize risk.

Equities have formed the foundation of long-term wealth creation for decades. At the same time, they are regularly exposed to periods of significant turbulence, triggered by monetary policy turning points, macroeconomic shocks, or abrupt shifts in market sentiment. For investors, such episodes mean not only temporary losses in wealth. They frequently also lead to procyclical investment decisions.

The classical response to severe drawdown periods follows two patterns: either investors turn to options to hedge portfolios, or they reduce their equity allocation when volatility rises. Both approaches have structural weaknesses. Options strategies incur continuous premium costs. Tactical risk reduction often reacts only after the bulk of a correction has already occurred, and then frequently misses the subsequent recovery.

Against this backdrop, an alternative approach is coming into focus: systematic defensive overlays deployed alongside strategic equity allocations. The core idea is compelling. While equity markets come under pressure during stress periods, other markets respond along the same macroeconomic shock channels but with countervailing moves. Declining growth expectations can support government bonds, industrial commodities price in cyclical slowdowns early, and gold gains when uncertainty rises.

Systematic multi-asset overlays leverage precisely these relationships. Rather than relying on a single source of protection, they combine multiple diversification channels within a rules-based approach across liquid futures markets in government bonds, commodities, currencies, and precious metals. Positioning follows not discretionary market views, but quantitative signals: relative momentum indicators, changes in volatility and correlation structures, or the dispersion of trends across different markets.

Unlike tail hedge strategies, the protection does not rest on convex option profiles but on dynamic adjustment of market exposure. While options can generate large gains during turbulent periods but incur ongoing costs, multi-asset overlays tend to produce more linear return profiles across multiple markets. Macroeconomic forces that weigh on equities often simultaneously favor other asset classes.

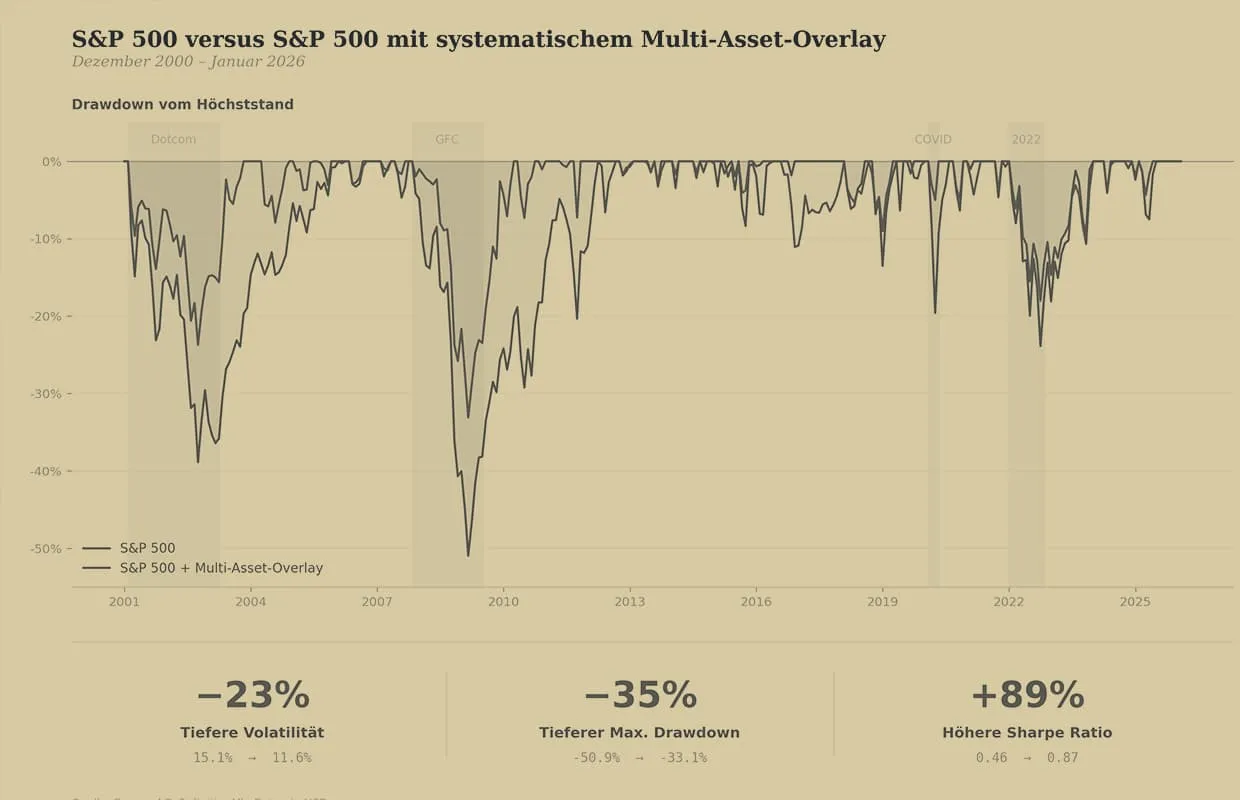

Simulations using liquid futures markets dating back to the early 2000s show that a diversified cross-asset overlay can reduce the volatility of a global equity portfolio by 20 to 30 percent. Historical maximum drawdowns can be reduced by approximately one third, while the majority of long-term equity returns is preserved.

This perspective is gaining relevance particularly now. Global equity indices are increasingly concentrated. In the United States, a substantial share of index weighting is attributable to a handful of large technology companies. At the same time, government bonds are more sensitive to inflation developments and monetary policy uncertainty. In such a market structure, diversification across asset classes alone is no longer sufficient.

Systematic alternatives pursue the goal of isolated alpha generation less than they aim to alter the structure of portfolio risk: smoothing volatility, cushioning drawdowns, and reducing dependence on individual market segments.

In a world increasingly shaped by macroeconomic regime shifts, geopolitical tensions, and structural market dislocations, the role of such systematic multi-asset strategies in strategic portfolio allocation is likely to grow further in importance. Everon develops systematic multi-asset strategies for asset managers and institutional investors seeking to manage their equity risk more intelligently.

This article is for general information purposes only and does not constitute investment advice or an offer to buy or sell financial instruments. Everon AG is a wealth manager licensed by FINMA under FinIA. Past performance is not a reliable indicator of future returns.