At present, movements on the stock markets are strongly influenced by current developments, including the war in Ukraine, tensions in international relations and the sharp rise in interest rates due to high inflation.

In order to better understand the interrelationships, it often helps to take a look at the past, which is why we would like to take a closer look at these in a review of the year 2022.

Contents

- 1 Rising inflation from 2021

- 2 Central banks react with interest rate hikes

- 3 What was the impact at Everon?

- 4 Which factors were good in 2022 and which were not?

- 5 Challenges 2023

- 6 Which sectors are interesting?

- 7 Continued focus on the momentum and quality factors

- 8 Which regions are interesting?

- 9 Summary

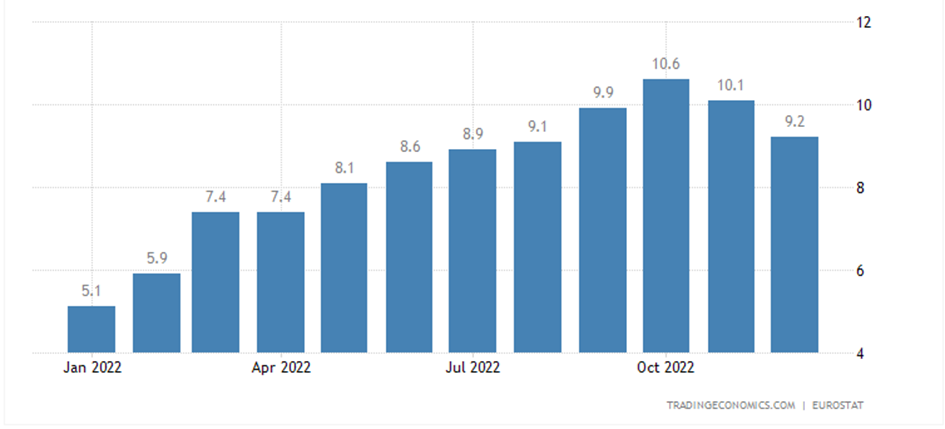

Rising inflation from 2021

In 2021, we still saw exceptionally good returns spurred by the further easing of the Corona crisis and global supply chains. As early as 2021, inflation in the US and also in Europe started to pick up and exceed the target rate of 2.0%. However, central banks did not see the need to intervene as inflation was seen as «transitory», i.e. only temporary. The expectation was that it would fall again as soon as the global economy normalized.

As we now know, this was not the case. The main reason for the high inflation was a sharp increase in demand for goods while supply could not keep up. This resulted in rising prices of raw materials and transportation, which in turn increased the production costs of companies.

When it became clear at the beginning of 2022 that inflation would continue to rise and the Ukraine crisis would worsen, the global financial markets corrected sharply. Growth stocks were hit particularly hard as market participants shifted from growth to value. This is mainly due to the fact that growth stocks are more vulnerable to general economic fluctuations and are often significantly leveraged. The expected increase in interest rates would therefore hit these companies particularly hard, as their financing costs would rise. The oil price also rose in March to a level of just under USD 128, which was only higher in the last 22 years at the time of the financial crisis.

Central banks react with interest rate hikes

At the beginning of March, the U.S. Federal Reserve raised interest rates for the first time by 0.25 percentage points. This marked the beginning of the steepest rate hike cycle in history.

In the months that followed, it then became clear that central banks around the world would aggressively raise rates in 0.50 to 0.75 increments to combat surging inflation. As a result of the rising interest rates, bond prices fell at the same time as equity prices. The stock market was rather burdened here by the fact that there was a risk of recession due to strong interest rate hikes. This was also a particular drag in 2022: bonds and equities, which are normally combined because they have a very low correlation, were now running in lockstep. The Swiss investment grade corporate bond index SBI, lost almost 12 percent in 2022, which is the biggest loss since the financial crisis.

Reading tip: The Evolution of the Correlation Between Stocks and Bonds

What was the impact at Everon?

At the end of 2021, our portfolios were still focused on growth, which had also given us an exceptional return in 2021. Then the relatively quick switch from growth to value at the beginning of 2022 cost us quite a bit of return right in the first month. Thus, January was also the worst month for us in the entire year.

Since our factor investing strategy is clearly systematic and focused on a long investment horizon, we do not try to time the market. So we adjusted our portfolios step by step to the changing market conditions, especially in terms of sectors. However, as there was a lot of uncertainty and volatility in the markets, especially in the first half of 2022, almost all sectors except the energy sector suffered due to rising energy prices. This ensured that the adjustment of the sectors did not have an immediate effect.

Our approach and avoidance of market timing also implies that we maintain Strategic Asset Allocation and do not actively overweight or underweight asset classes. We maintain a broadly diversified portfolio across many sectors and currencies even during times of crisis. The permitted ranges per sector and currency, however, may change depending on market conditions. All these measures are also aimed at keeping portfolio turnover and value fluctuation under control.

Since we always trade at certain intervals and our approach also has a certain short-term lag to fast events in the market, we accept certain movements in the market before steering against them. And even then, we make adjustments gradually, because our goal is not to time the market, but to achieve a high risk-adjusted return at all times. Reacting extremely to short-term developments increases the risk of «chasing the market», which comes from trying to time the market.

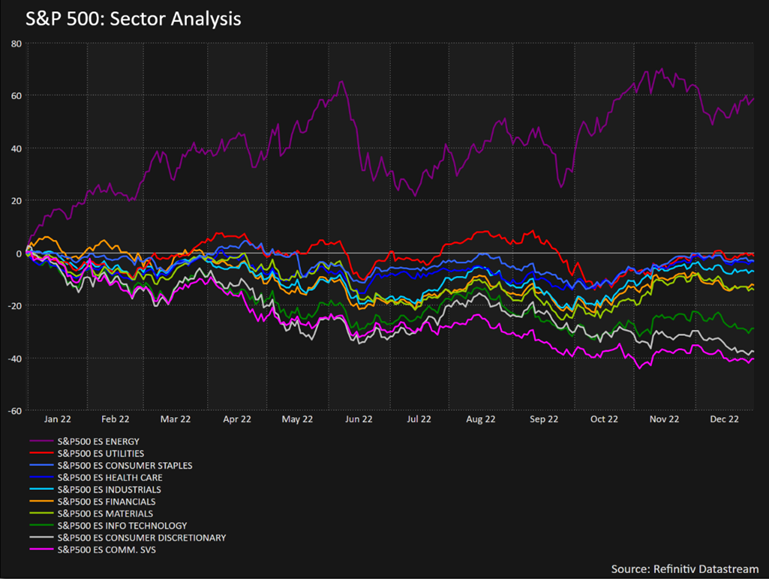

How did different sectors perform in 2022?

As we can see from the example of the S&P 500, consumer cyclicals, real estate, technology and telecom in particular lost a lot of value last year. This is not surprising, because consumer cyclicals are the first to suffer from a slump in consumer demand (which is what interest rate hikes are also trying to achieve), real estate companies have higher financing costs, and technology and telecom contain a large share of growth stocks and are sensitive to economic fluctuations.

Consumer staples, energy, healthcare and industrials were the best performing sectors in the S&P last year. These sectors are known to be defensive, which is why we want to focus on them again next year.

Which factors were good in 2022 and which were not?

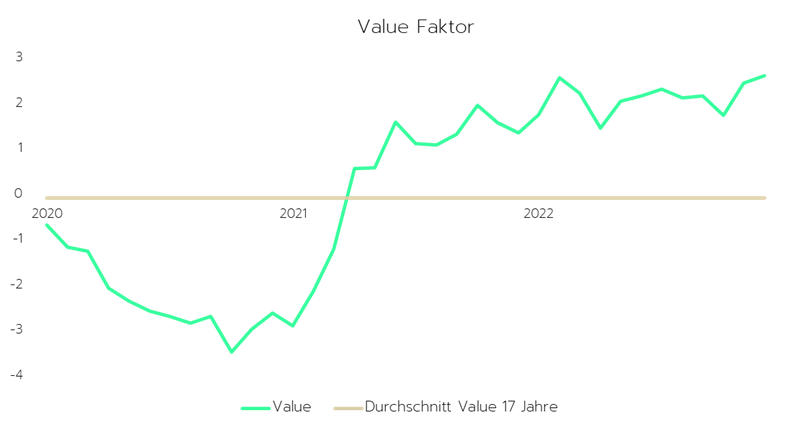

The value factor, which focuses on the ratio of market to book value of a stock, is a clear winner of the last year. This makes sense, as this factor is used to buy stable and established companies that have relatively cheap valuations. However, this factor has performed rather moderately over the last 17 years.

The quality factor focuses on the operating profitability of a company and initially performed well, but tended to decline again in the second half of the year. This also speaks for the crisis mode that prevailed in the market. However, this factor also ensures an excess return in the long term.

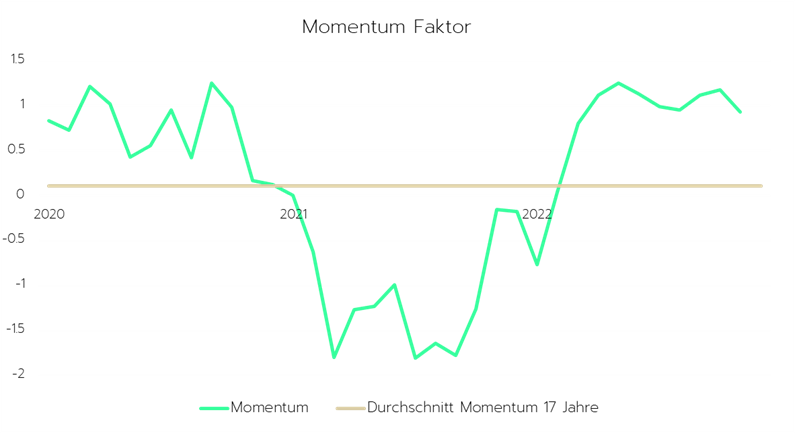

The momentum factor turned from negative to positive last year. This can be explained by the fact that in simultaneously falling markets, the stocks that previously had good momentum lose more, as profits are more likely to be taken here. With the calming of the markets in the middle of the year, the momentum factor also works better again. This factor also ensures an excess return in the long term.

One factor that has given us an excess return in the past, but has contributed negatively in 2022 in particular, is the size factor. This factor gives us a higher weighting in small- and mid-cap stocks over the long term, which suffer more in times of crisis but perform better in normal times.

From the long-term implications mentioned above, the factors Momentum and Quality have the largest weightings in our model. However, these are finely adjusted on a monthly basis and adapted to developments. Again, we have the long time horizon in mind.

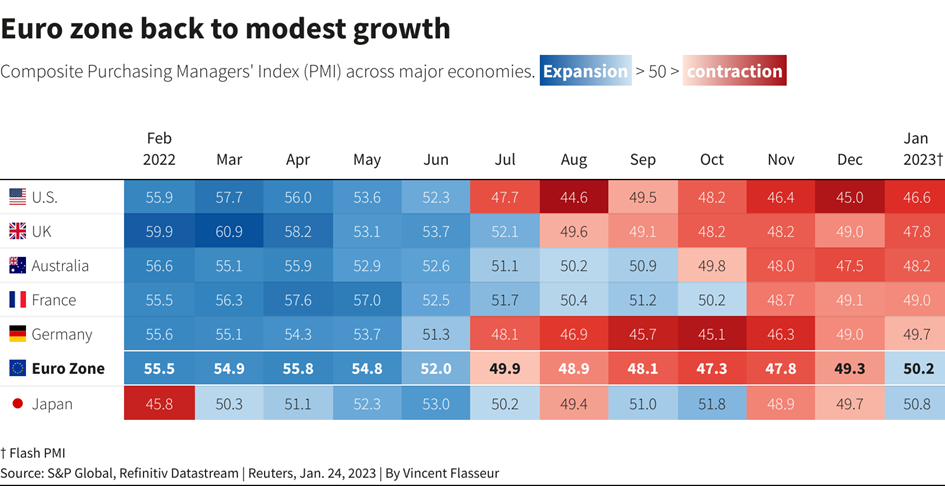

Challenges 2023

The year 2023 has started surprisingly well and we saw one of the strongest January rallies in recent years. Market participants assumed that interest rates would peak this March. However, recently released inflation and labor market numbers have turned unexpectedly «hot» again. This in combination with the rhetoric of the central banks has led to the markets becoming increasingly uncertain again about the end of the interest rate cycle. For this reason, we are currently seeing higher volatility in the markets again.

So far, all scenarios are still open, even the scenario of a so-called «soft landing», i.e. a minor impact on the economy due to increased interest rates, is still considered possible. In Europe in particular, economic indicators show a rather positive picture, with the probability increasing that a recession can be avoided here in 2023. However, the inverted yield curves in Europe and the U.S. indicate a recession, but no one knows exactly when and how severe it will be.

The current reporting season showed what many had already expected: The outlook of companies for this year is becoming increasingly gloomy. Many companies are experiencing further pressure on their margins because they cannot continue to pass on the high production or acquisition costs to customers on a one-to-one basis. In this way, they would risk a decline in demand that is too high. For example, the current Q4 2022 reporting season of S&P 500 companies was the second-worst since the 2008 financial crisis in terms of companies reporting positively above market expectations (Source: Earnings Insights February 17, 2023 by FactSet Research Systems Inc.). This suggests that analysts have not yet correctly revised their expectations downward.

In general, the first half of 2023 is expected to remain challenging and volatility is expected to remain elevated. The fact that market participants do not yet know exactly how strong the impact of high interest rates will ultimately be means that any positive or negative news can cause significant movement in the market. In the second half of the year, we expect that the market will then tend to move sideways or slightly upwards, as by that time far more information will be available on how the high interest rates will impact accordingly.

It is still important to remain cautious and not to be deceived by interim rallies.

Which sectors are interesting?

The financial sector is also affected by the risk of a recession, although this sector traditionally benefits from higher interest rates. Large financial institutions are massively increasing their loan provisions for potential loan defaults. Also, a recent quarterly report from a major credit card company in the U.S., shows that customer repayment behavior continues to deteriorate. This may be an indication that the default rate may increase, especially in the consumer credit sector. Nevertheless, this sector remains interesting for 2023, but it is important to focus on large and stable institutions (quality factor).

We also see the consumer staples and industrial sectors as good sectors for 2023, firstly because they are defensive sectors and secondly because they have been showing good momentum since last fall. The industrial sector is benefiting from the fact that the feared energy crisis has so far failed to materialize and commodity prices have leveled off again.

We tend to underweight the technology sector, as it is very volatile and highly sensitive to macroeconomic changes. We are also avoiding an excessive weighting in consumer cyclicals and real estate companies. These are weighed down by falling consumption on the one hand and high interest costs on the other.

However, in each sector there are individual stocks that may look attractive, it is just a matter of identifying them and investing in them, which is possible with our investment approach in direct investments. For this reason, we do not exclude any sector per se. For 2023, it is even more important to keep a broadly diversified portfolio, which is spread across sectors and currencies.

Continued focus on the momentum and quality factors

In 2023, we will continue to focus on the factors Momentum and Quality, as this combination is advantageous. Through Momentum, we identify those companies whose share price is starting to recover (positive momentum). Through Quality and other factors such as Risk or Value, we select those companies that have some substance. In this way, we focus the portfolios on quality and the lowest possible risk.

Which regions are interesting?

We believe our focus on Swiss equities will be particularly helpful in the first half of the year. As a country with low inflation and a stable economy, this brings a certain stability and quality to our portfolios. Also from a currency risk perspective, this makes perfect sense. North America and Europe will continue to be our main markets, but with an increased weight on Europe, as we have seen good momentum there again since last fall and the EUR is also gaining strength again. This is mainly due to the fact that company valuations in Europe appear more attractive, gas prices have fallen massively again and economic indicators are also proving to be more stable than in the US. In the USA, the indicators tend to deteriorate, whereupon earnings expectations will probably still have to be adjusted downwards a little in the first half of the year, which may lead to price losses.

Summary

The first half of 2023 remains challenging. We are focusing on more defensive sectors and keeping an eye on our Momentum, Quality, Size and Risk factors.

We see Europe and Asia as more attractive than the US and will adjust our foreign bias accordingly. It remains important to diversify well across regions, currencies and sectors, without betting too much on any single area. It is still important to maintain a long-term focus, which is why we remain true to our systematic strategy and adherence to asset allocation.